Digital Customer Onboarding in Banking: How to Reduce Risk

In the past, opening a bank account meant standing in line at a branch, filling out stacks of forms, submitting identification documents, and waiting days, or even weeks, for approval. Today, customer onboarding in banking has evolved far beyond physical visits. Financial institutions now leverage digital solutions to streamline the process, reduce operational costs, and offer faster, more convenient access to products and services.

Yet, the shift to digital onboarding brings its own challenges, particularly for compliance professionals tasked with meeting KYC (Know Your Customer), AML (Anti-Money Laundering), and other regulatory obligations. Balancing regulatory adherence with a seamless customer experience is critical.

The Evolution of Customer Onboarding in Banking

Digital onboarding in banking didn’t appear overnight. Banks first introduced online services in the 1980s, primarily for basic account access. By the mid-1990s, many major banks offered websites enabling customers to check balances and even open accounts online. Over the following decades, technology improvements, such as mobile apps, secure document scanning, and AI-driven identity verification transformed onboarding from a manual, paper-heavy process into a rapid, largely automated experience.

Today, most customers can complete onboarding in minutes from their devices. While this convenience enhances adoption, it also introduces risks that financial institutions must actively manage.

Key Risk Areas in Digital Onboarding

Compliance officers need to understand the primary risks in onboarding in financial services:

Data Security and Privacy: Customers trust banks to safeguard sensitive personal information. Mishandling or breaches can lead to financial loss, regulatory penalties, and erosion of trust. Compliance officers must ensure onboarding systems meet standards such as GDPR, CCPA, or local privacy laws.

Identity Fraud and Impersonation: With data breaches and phishing attacks on the rise, verifying that a customer is who they claim to be is more important than ever. Synthetic identities, created from stolen or fabricated information, pose a growing threat to banks.

Regulatory Compliance: Banks must comply with complex, evolving frameworks like the Bank Secrecy Act, AMLD6, FATF recommendations, and local regulations. Failing to meet these requirements can result in hefty fines, reputational damage, and audit failures.

Effective Risk Reduction Strategies

Banks can mitigate these risks while enhancing customer experience through several key strategies:

AI and Machine Learning for Fraud Prevention: AI-powered tools can automatically scan IDs, compare biometric data, and detect anomalies in real time. This reduces the chance of fraudulent accounts slipping through and accelerates the approval process.

Digital KYC and AML Implementation: Automated KYC and AML checks allow institutions to verify identities quickly without compromising accuracy. Advanced solutions flag high-risk customers and reduce the burden of manual review.

Enhanced Due Diligence (EDD): For customers or transactions with elevated risk, EDD ensures additional verification steps are applied, reinforcing compliance with regulations and minimizing exposure to fraud.

Streamlined Onboarding Workflows: Simplifying forms, enabling digital signatures, and maintaining transparency throughout the onboarding journey reduces friction, lowers abandonment rates, and improves customer satisfaction.

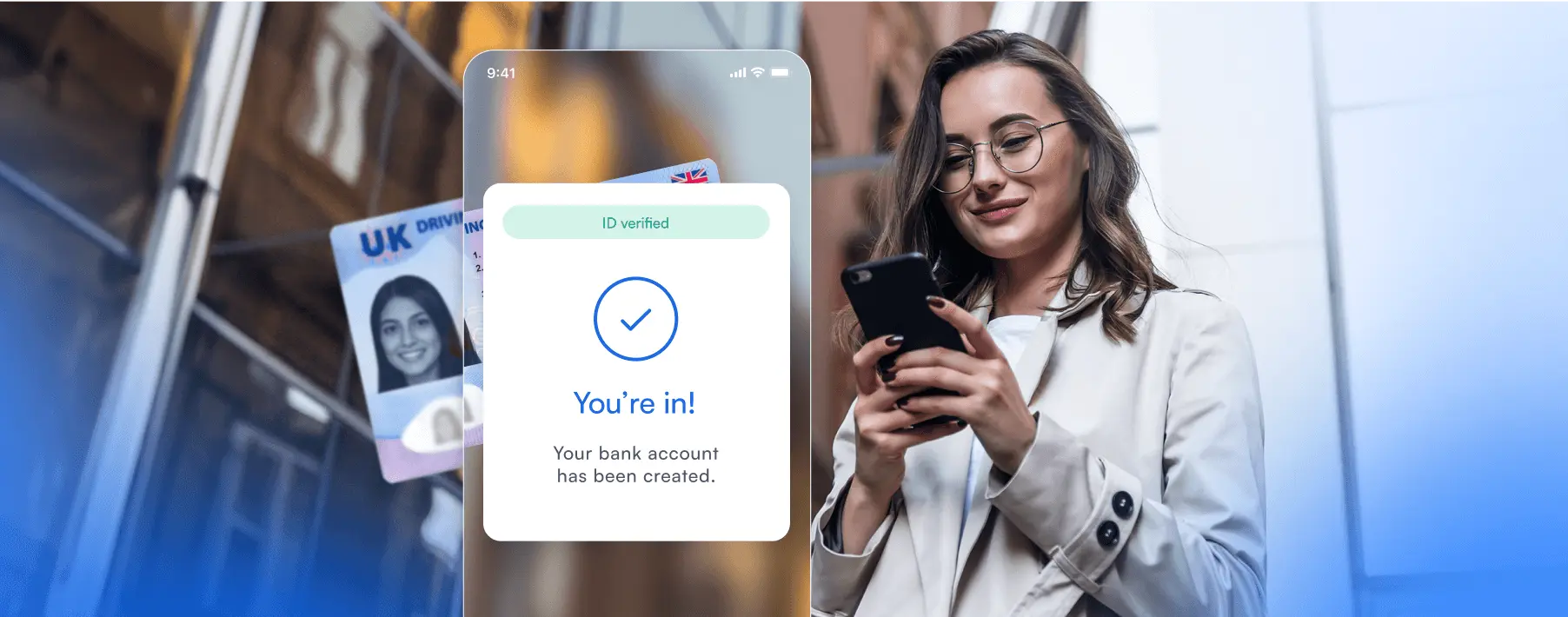

Digital Onboarding Workflow: Step by Step

A typical modern digital onboarding process incorporates multiple layers of verification, while keeping the customer journey frictionless:

Approval and Account Creation: Verified customers are onboarded, and account access is granted within minutes instead of days.

Data Capture: Customers enter personal information and upload identity documents using secure digital channels.

Document Verification: OCR (Optical Character Recognition) technology extracts and validates data from passports, driver’s licenses, or national IDs.

Biometric Verification: Face matching and liveness detection ensure the person submitting the ID is its rightful owner.

Automated Risk Checks: AI systems cross-reference databases and watchlists to identify potential fraud or high-risk profiles.

Measuring Success: Metrics That Matter

Compliance teams can evaluate onboarding effectiveness with metrics like:

- Average onboarding time (minutes instead of days)

- Abandonment rates (reduction after streamlining forms)

- Fraud detection rate improvement

- Reduction in manual review workload

These benchmarks not only ensure regulatory compliance but also provide tangible evidence of operational efficiency.

The Role of Technology in Compliance and Customer Experience

Microblink’s integrated identity platform offers a comprehensive solution for customer onboarding in banking. By combining OCR, AI-driven document verification, and biometric checks, the platform ensures rapid and secure identity verification. Banks can verify customer IDs in seconds, significantly reduce drop-off rates, and minimize manual reviews, thus helping compliance professionals maintain audit readiness while enhancing the customer experience.

For example, Banco Azteca in Mexico uses Microblink to scan IDs and passports during onboarding. According to Francisco León, IT Director at Banco Azteca, customers are “really delighted by the implementation because it’s such a simple and easy solution to scan IDs.”

Best Practices for Compliance-Focused Onboarding

- Prioritize Regulatory Alignment: Ensure all onboarding steps comply with local and global KYC/AML regulations.

- Educate Customers on Digital Safety: Clear guidance reduces risk and fosters trust.

- Monitor and Adapt: Regulations evolve constantly; onboarding processes must be flexible to maintain compliance.

- Leverage Automation Wisely: Use AI and digital tools to reduce human error, speed approvals, and maintain robust risk controls.

Manual vs. Automated Onboarding: A Quick Comparison

| Feature | Manual Onboarding | Automated Digital Onboarding |

|---|---|---|

| Average Time | Hours to days | Minutes |

| Fraud Detection | Reactive, human-dependent | Proactive, AI-driven |

| Compliance Checks | Manual, error-prone | Automated, auditable |

| Customer Experience | Friction-heavy | Frictionless |

| Operational Costs | High | Lower |

Reduce risk and accelerate growth with Microblink

Banking technology has undergone significant advancements since the 1980s, when it first appeared on a wider scale. However, these advancements have been accompanied by new threats, risks, and regulatory standards. To stay competitive and compliant, banks and financial institutions need to continually innovate and adjust to changing regulations and market demands.

Improvement and adaptation are key when it comes to digital customer onboarding in banking. This includes integrating the latest technologies, which offer advantages over competitors and deliver a superior customer experience. Microblink can help. Contact us to learn how to simplify your onboarding process.