Retail Banking Customer Onboarding Process: Stop Fraud Without Killing Conversions

Designing a retail banking customer onboarding process has never been more difficult, or more critical. Product managers must balance KYC/AML compliance, synthetic identity risk, and rising user expectations, all while keeping conversion rates healthy. The result is a workflow that needs to be secure, fast, intuitive, and adaptable.

This guide breaks down the key steps in the financial services onboarding process, the regulatory requirements you need to meet, and best practices for verifying identities, reducing fraud, and improving user experience. It also explains how Microblink’s identity platform supports retail banks with speed, accuracy, and compliance-ready automation.

What Is the Retail Banking Customer Onboarding Process?

The onboarding process is the set of steps a new customer must complete to open a retail banking account: from identity verification to risk checks to account creation. Done well, onboarding becomes a strong first impression. Done poorly, it becomes a major source of fraud losses, abandonment, and regulatory exposure.

The Step-by-Step Digital Customer Onboarding Workflow

1. Identity Capture

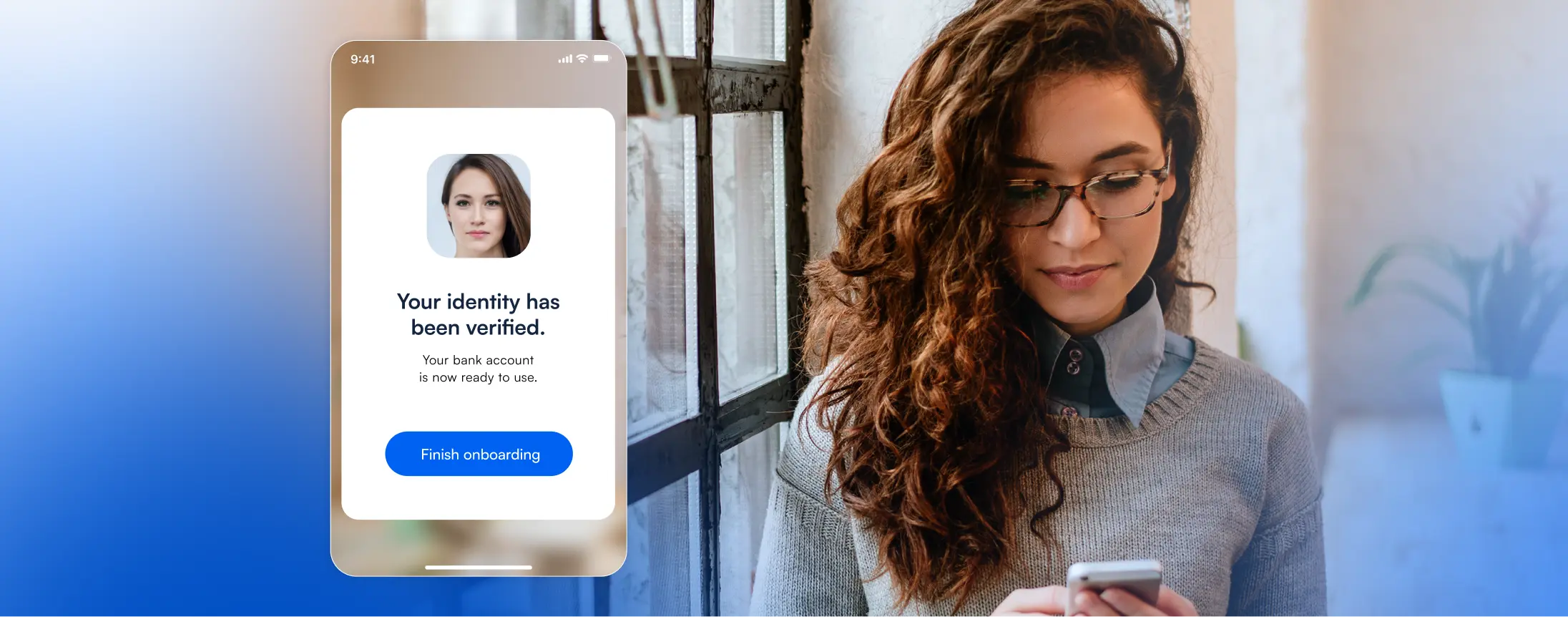

Customers upload a government ID, take a selfie, or provide required personal data. Modern onboarding requires mobile-first capture with real-time guidance to reduce drop-off.

2. Identity Verification

Banks must verify:

- The document is authentic

- The person is who they claim to be

- The applicant isn’t using a synthetic or manipulated identity

Microblink automates all three with AI-powered document analysis, biometric matching, and fraud signals that detect deepfakes and fabrications in milliseconds.

3. KYC/AML & Screening Checks

This includes:

- Sanctions & watchlist screening

- PEP checks

- Adverse media

- Risk scoring

Automation keeps these steps fast while maintaining fully auditable compliance trails.

4. Account Creation & Customer Profiling

Once verified, users create credentials, set preferences, and enter your CRM.

Banks often integrate this step with cross-sell flows or early personalization.

5. Ongoing Monitoring

Onboarding doesn’t end at account opening.

Risk scoring, transaction checks, and customer re-verification workflows maintain compliance and reduce fraud over time.

How to Ensure Compliance With KYC/AML Regulations

Product managers must design onboarding workflows that meet strict regulatory standards without adding unnecessary friction.

Best practices include:

- Automating ID checks with AI/ML to reduce human error

- Creating audit-ready logs for every verification attempt

- Implementing risk-based KYC to avoid punishing low-risk customers

- Building configurable review and escalation paths for borderline cases

Microblink supports all of the above with a fully integrated identity platform that automatically records verification steps for compliance review.

Reducing Onboarding Friction Without Compromising Security

High abandonment and false rejection rates are common pain points for retail banks.

To solve this, product managers should focus on:

Real-Time UX Guidance

Prompts that help customers correct blurry images, missing fields, or selfie mismatch prevent unnecessary failures.

Adaptive Verification

Risk-based controls apply stricter checks only when needed, lowering friction for legitimate applicants.

Automation + Human Review Only When Required

A hybrid workflow reduces false rejects by letting teams intervene only in edge cases.

Mobile-Optimized Workflows

The majority of onboarding now happens on mobile devices; slow or clunky flows directly cost you customers.

Microblink’s risk-adaptive verification helps banks reduce friction and fraud by adjusting checks based on document quality, device risk, and behavioral signals

Stopping Synthetic Identity Fraud During Onboarding

| Threat / Challenge | What It Looks Like in Retail Banking | How to Detect It | How Microblink Helps |

| AI-generated or manipulated IDs | Applicants submit documents that look real but contain fabricated or AI-forged fields. | AI-based document forensics, texture analysis, tamper pattern detection. | Microblink flags pixel-level abnormalities and detects document fabrication in milliseconds. |

| Deepfake or spoofed biometrics | Fraudsters use masks, injections, or deepfake videos to bypass selfie verification. | Biometric liveness checks and motion-based challenge–response. | Microblink’s advanced liveness detection blocks spoofed selfies and model-driven attacks. |

| Synthetic assemblies of real + fake data | Name, SSN, DOB mixed from multiple sources to appear legitimate. | Cross-data correlation, behavioral analytics, high-risk identity signals. | Microblink surfaces risky identity patterns missed by static databases. |

| Mismatched user behavior | Interaction patterns, device signals, and velocity don’t match a normal new customer profile. | Behavioral analytics, device fingerprinting, anomaly scoring. | Microblink uses behavioral and device risk intelligence to spot suspicious session activity. |

Reducing False Rejection Rates (Without Opening the Door to Fraud)

False rejections quietly erode trust long before fraud losses ever show up in your metrics. Product managers feel this most acutely during onboarding: customers complete the entire flow only to be declined due to poor image quality, rigid risk thresholds, or overly strict verification rules. Reducing these false failures doesn’t require lowering security, it requires smarter, more adaptive signals. Techniques like ML-driven risk scoring, real-time error correction during image capture, and configurable decisioning rules help banks keep legitimate customers in the funnel while preserving strong fraud barriers. Microblink’s verification engine enhances pass rates by combining document forensics, biometric matching, and quality scoring to allow more good users through without increasing exposure.

Re-Onboarding and Remediation: A Better Way to Handle Verification Failures

Verification failures don’t have to mean lost customers. Too many banks treat a failed attempt as the end of the journey, rather than an opportunity to recover a legitimate user. A strong remediation workflow offers clear explanations, guided retry steps, and automated document retake flows to correct simple mistakes. For more complex cases, support teams need escalation paths that don’t create compliance gaps. Microblink helps banks design structured re-onboarding experiences that maintain auditability while giving customers a fair, consistent chance to complete verification successfully and dramatically reducing abandonment.

Accessibility & Inclusion as Core Drivers of Onboarding Success

Accessible onboarding is now an expectation from regulators and customers alike. Retail banks must design flows that support multiple languages, screen readers, high-contrast visuals, and simplified instructions for users with cognitive or physical challenges. Mobile optimization is equally essential, especially in markets where customers rely on lower-end devices or inconsistent network speeds. By building inclusivity into onboarding from the start, banks expand their addressable market and remove friction points that disproportionately impact legitimate customers. Microblink’s mobile-first design, clear real-time guidance, and flexible SDKs support inclusive experiences across a wide range of devices and accessibility needs.

Why Microblink?

Microblink helps retail banks design onboarding workflows that are:

- Fast (sub-second checks)

- Accurate (advanced document forensics + biometrics)

- Compliant (audit trails + KYC/AML integrations)

- Fraud-resistant (synthetic identity detection built in)

- User-friendly (real-time guidance, mobile-first design)

With a single platform and flexible APIs, Microblink empowers product teams to reduce friction, stay compliant, and unlock higher customer acquisition. Get in touch today to learn more.