How Automated KYC Reduces Friction in Fraud Detection

Financial institutions and digital businesses are tasked with two seemingly antithetical obligations: protecting their customers’ data and providing a seamless user experience.

Why antithetical? A handful of manual identity verification measures—multi-factor authentication, one-time passwords, and delivering paperwork in person—are widely viewed as burdens by the customer.

This can result in greater friction in onboarding and transaction processes—and the diminished conversions, reduced retention rates, and increased drop-offs that may arrive with it.

This is where automated know your customer (KYC) serves as an increasingly attractive solution. In this article, we’ll examine how automating KYC processes benefits businesses and customers in the battle against fraudulent activity.

What is KYC?

Performed to prevent identity theft, money laundering, and financial crimes before they occur, regulated industries—such as banking, alcohol, travel, tourism, and gaming—are legally required to comply with KYC regulations. That said, nearly every business may profit from adhering to KYC guidelines because of the confidence it can foster and the financial protection it offers.

How do KYC regulations relate to anti-money laundering (AML) laws?

The concept of KYC fraud detection dates back to the Bank Secrecy Act (BSA) in the 1970s—a set of regulations and laws developed to counter the risk of financial terrorism, money laundering, and other illegal activities.

Anti-money laundering (AML) laws stemmed from this. KYC compliance is an imperative component of these laws. To remain compliant, financial organizations and additional industries must execute ongoing monitoring and flag (and report) any suspicious activity.

Drawbacks of traditional KYC methods

Traditional KYC methods—such as providing an institution with physical documents like a utility bill—may have been acceptable before the digital age. In our accelerated era, however? Not so much.

The primary pitfalls of traditional KYC methods come down to:

- Decreased customer satisfaction: A recent survey reveals that 82% of customers expect a smooth and simple digital experience. Manual KYC measurements interfere with this. Largely deemed as a time-consuming hindrance, it can delay onboarding and negatively affect a customer’s perception. As digital banks become increasingly popular, this has significant implications in the financial services sector.

- Increased risks: Manual KYC methods (and the data entry required) are subject to human errors and inconsistencies, which may render financial organizations and other businesses vulnerable to fraud and compliance missteps. Further, organizations that store physical documents may place data security and privacy at risk; breaches could be fatal to an institution’s reputation and ultimate success.

- Elevated costs: Traditional KYC procedures naturally call for human labor. This can be tremendously costly for organizations requiring large volumes of identity verifications while handling KYC protocols. Moreover, failing to comply with KYC regulations—which have become progressively more rigorous and nuanced amid growing financial crimes—comes with hefty fines: in 2021 alone, several US financial organizations accrued $2.7 billion in penalties for not meeting KYC and AML regulations.

- Reduced scalability: Relying on manual KYC methods impacts an organization’s capacity to scale. This can unnecessarily stunt a company’s growth, as automated KYC processes are readily available—a topic we’ll turn to next.

The role of automated KYC in reducing friction

In sum, using technology such as AI to verify a legitimate customer’s identity can significantly curb friction in onboarding and transactional processes by saving both businesses and customers time and effort. This is key across the board, especially in industries where swiftness and ease are fundamental.

Benefits of automated KYC in fraud detection

Automated KYC verification processes have a host of advantages, namely:

- Decreased operational costs: As discussed, traditional KYC methods require internal staff members to not only conduct identification processes but also remain on top of changes in KYC regulations. Automated KYC shrinks labor and other overhead costs, empowering organizations to realize their growth potential (and boost their bottom line).

- Lowered risks: Automated KYC provides perpetual monitoring in real-time. This enables institutions to spot activity that may be indicative of financial fraud (and other illicit activities) promptly and effectively.

- Enhanced customer journey: Organizations and businesses that offer timely, frictionless experiences are more likely to satisfy—and retain—customers.

KYC technologies and innovations

We’re just beginning to uncover the world of automated KYC options. To date, however, the most prevalent technologies and innovations include:

- AI/ML, which can review enormous datasets and analyze them for patterns and deviations

- Liveness detection, which can conduct facial movement evaluations to confirm a customer’s identity

- Document verification, which checks a customer’s identity through capturing, extracting, and certifying identification documents (such as a passport)

Voice biometrics, facial recognition, and behavioral biometrics are also employed.

What do companies need to know about implementing KYC procedures?

KYC is broken down into three phases for banks and other financial institutions:

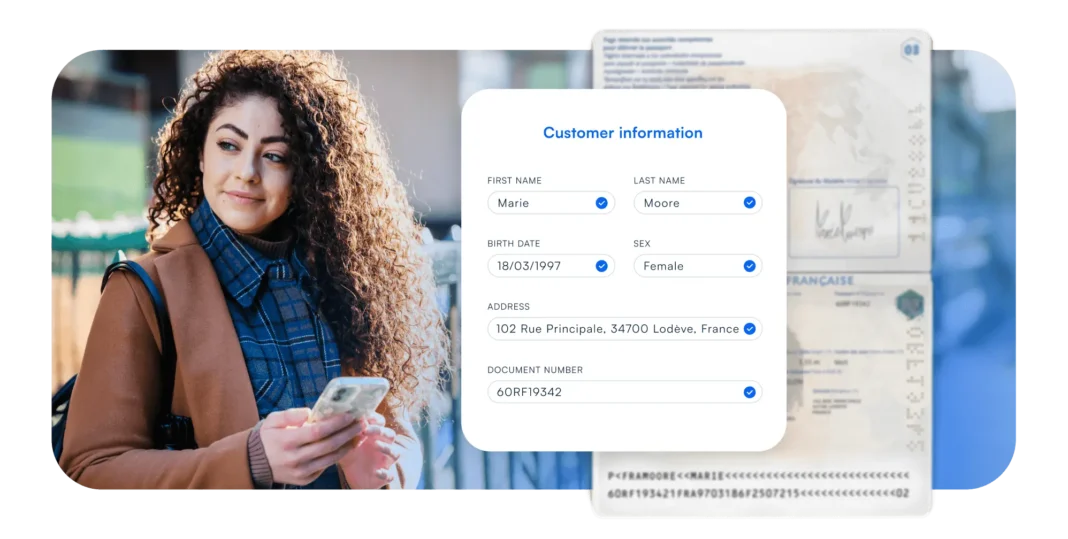

- Customer identification program (CIP): CIP accounts for essential information needed for identity verification. This data is contingent upon the jurisdiction, but it typically involves verifying the customer’s name, address, date of birth, and a government-issued identification number (such as their driver’s license number).

- Customer due diligence (CDD): Simply put, CDD assesses a customer’s risk factor to an organization, primarily in terms of fraudulent schemes, all of which can undermine an institution’s financial success and reputation.

- Enhanced due diligence (EDD): EDD is the most stringent form of due diligence. Conducted with high-risk customers—such as a politically exposed person (PEP)—it helps institutions make savvy choices about onboarding customers and establish measures to manage potential risks.

How can you streamline KYC implementation?

Automated, AI-powered KYC conducts the most vital elements of KYC with accuracy and speed, chiefly through:

- Document scanning

- Identification verification

- Risk assessment

Are there limitations to this? Yes.

Every case is unique, and some may be complicated. Yet, one of the beauties of AI/ML is that they are, at their crux, constantly evolving to adapt to challenges.

How to pick the right KYC fraud detection technology

Selecting the most effective and appropriate KYC fraud detection technology for your organization depends on your business requirements and the technology’s ability to help you scale. Additionally, you may want to analyze the technology’s user-friendliness, integration capabilities, and operational efficiencies. Microblink was designed with all of this in mind to give companies best-in-class experiences.

How Microblink Can Help

As one of the top KYC solution providers, Microblink is at the vanguard of automated KYC. Our BlinkID helps organizations like yours guarantee that people are who they claim to be through our document scanning and verification technologies.

This could streamline customer identity verification and mitigate fraud by as much as 50%, bolstering your ever-important business relationship with your customer—and granting you the chance to exceed your potential.

Consider automating with Microblink to streamline your KYC implementation and enhance fraud detection. Take advantage of our cutting-edge technologies by trying a demo today.