CIP and KYC in Banking

In 2020, the FBI received over 791,000 complaints of suspected internet crime. Among these complaints, the most common offenses reported were phishing, non-payment/non-delivery scams, and identity theft.

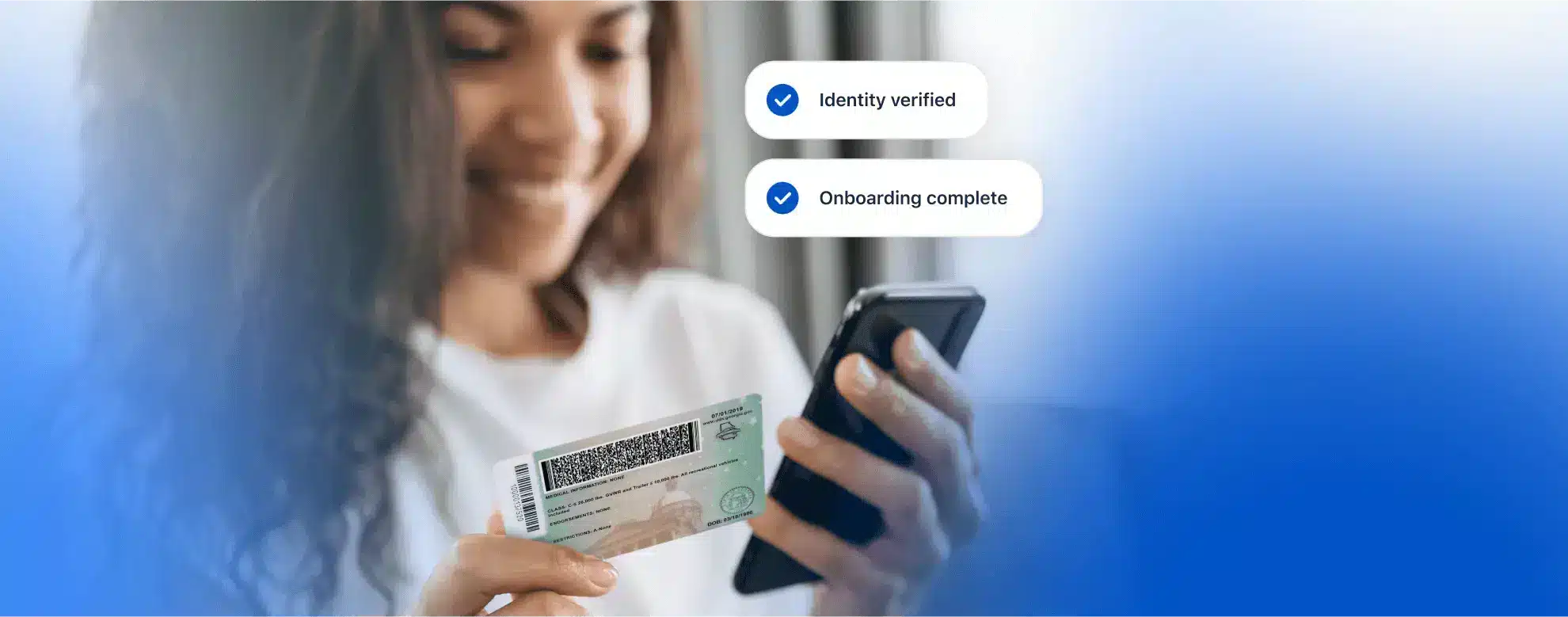

In this context, it becomes even more critical for financial institutions to ensure the security of their customers’ personal information through robust identity verification processes, such as the Customer Identification Program (CIP) and know your customer (KYC).

These programs are essential in creating a secure banking environment where identity verification is paramount. They help financial institutions verify the identity of their customers, prevent fraud, and comply with anti-money laundering regulations. By implementing these procedures, financial institutions can provide their customers with a sense of security and trust, which is crucial to maintaining a healthy and sustainable financial system.

What is CIP in Banking?

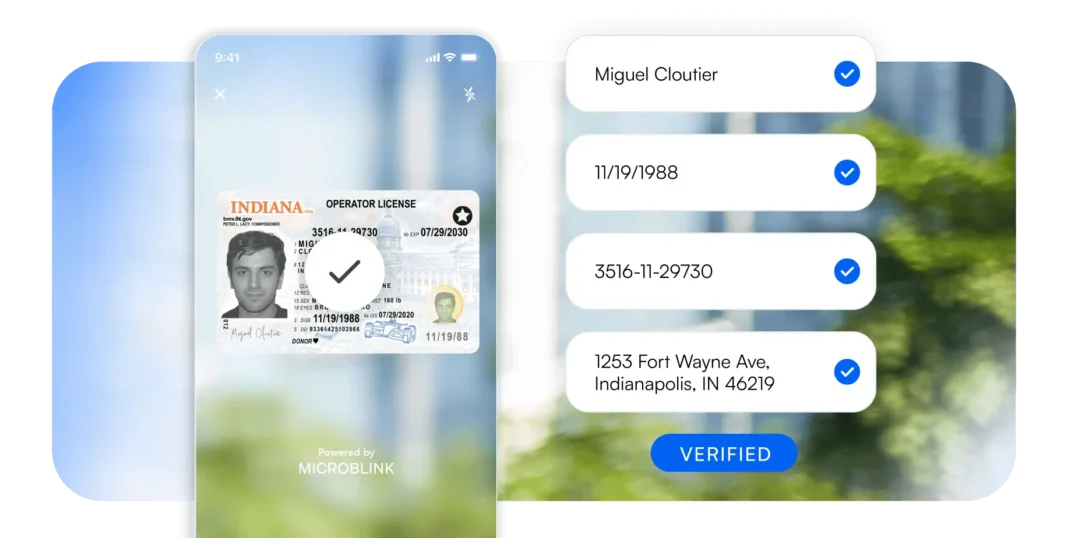

The Customer Identification Program is a legal requirement for banks and other financial institutions to verify the identities of new customers at account opening. The CIP’s purpose is simple but critical: create a reasonable belief that the bank knows the true identity of every account holder.

At minimum, CIP KYC processes require collecting and validating:

- Full legal name

- Date of birth

- Residential address

- Identification number (e.g., SSN or passport number)

Banks must verify this information using reliable, independent sources and document every step to meet audit standards.

Regulatory Requirements Around CIP

CIP is mandated under the USA PATRIOT Act, specifically Section 326. It requires financial institutions to implement reasonable procedures for verifying the identity of any person seeking to open an account to the extent reasonable and practicable.

This ensures the institution is not being used for financial crimes. The Bank Secrecy Act (BSA) also sets forth CIP requirements as part of its broader anti-money laundering (AML) policies.

Under the USA PATRIOT Act, the CIP requirement lays the groundwork for the fight against terrorism and money laundering. Financial institutions must have a CIP that includes procedures to verify the identity of individuals who open accounts, determine whether the individual appears on any lists of known or suspected terrorists, and notify the government of any discrepancies found during the verification process.

The Financial Crimes Enforcement Network (FinCEN) also plays a significant role in regulating and guiding the implementation of CIPs. As an agency of the US Department of the Treasury, FinCEN issues regulations and guidance to financial institutions, ensuring the practices for identity verification are consistent and effective across the board. It also enforces compliance with the BSA and the USA PATRIOT Act, ensuring financial institutions have adequate CIPs to thwart and report suspicious activities.

How CIP Fits Within KYC

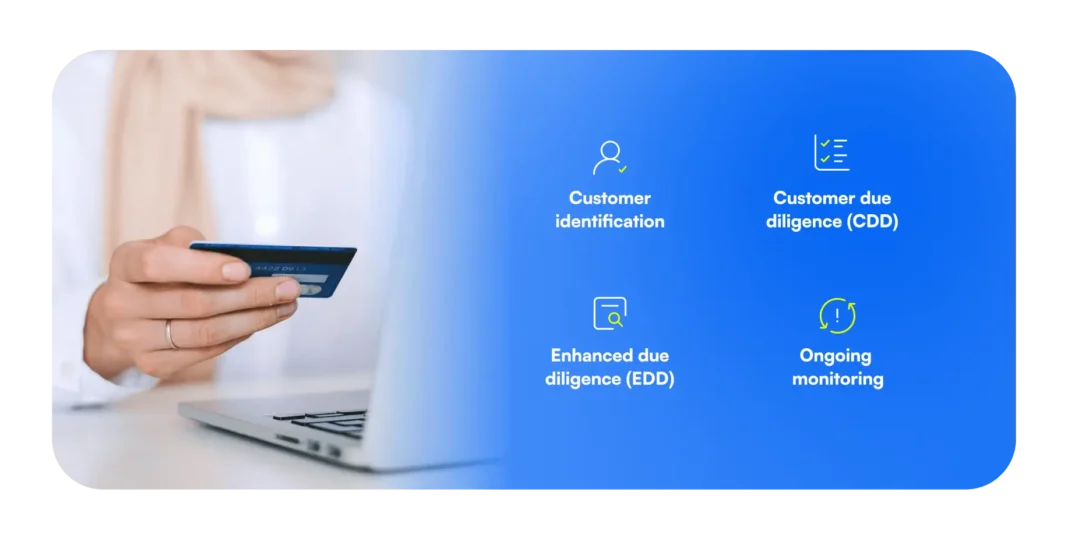

While KYC is the broader compliance framework that includes customer due diligence (CDD) and ongoing monitoring, CIP is the front gate.

CIP starts the moment a potential customer first interacts with your institution:

- Customer Identification (CIP) – Gather and verify identity data

- Customer Due Diligence (CDD) – Assess risk profile, monitor transactions accordingly

- Enhanced Due Diligence (EDD) – Apply deeper checks for higher-risk customers

- Ongoing Monitoring – Continuously watch for suspicious activity

Without a strong CIP, the rest of the KYC lifecycle is built on shaky ground.

The process for KYC includes four basic components:

- Customer identification: Collecting reliable, independent source documents, data, or information.

- Customer due diligence (CDD): Assessing the risk level of customers and monitoring their transactions accordingly.

- Enhanced due diligence (EDD): More intensive identity verification is needed for higher-risk categories.

- Ongoing monitoring: Continuously observing customer transactions to prevent deviations from their normal banking activities.

A real-world application of KYC is in the mortgage industry, where financial institutions must rigorously verify the identity of borrowers, understand their credit history, and continuously monitor payments to detect any signs of fraud or money laundering.

Differences between CIP in banking and KYC

While KYC encompasses a broad range of customer identity verification and risk assessment measures, CIP is specifically about establishing a reasonable belief that a financial institution knows the true identity of its customers.

The primary focus and scope are a bit different, too. CIP is the initial step in the customer onboarding process. It involves obtaining essential information such as name, date of birth, address, and identification number. The focus here is on creating a baseline for customer identity.

CIP is typically implemented during the account opening phase, while KYC extends beyond that, covering the entire relationship with the customer. Besides this, each set of standards has a slightly different goal.

CIP’s objective is straightforward: to verify the identity of new customers. KYC, however, aims to protect the financial system by preventing financial crimes and ensuring customer transactions align with their profile.

Overlapping elements between CIP and KYC

Both the customer identification programs and KYC frameworks are critical components in safeguarding the integrity of the financial institution and its customer base. The overlap lies in their shared goal of accurately identifying customers.

Integrating these elements heightens the effectiveness of both CIP and KYC, ensuring a robust defense against the illicit use of the financial system. This synergy helps create a secure banking environment resilient to fraud and financial crime.

Importance of CIP and KYC in banking

Both CIP and KYC are foundational elements for securing financial operations and preserving the integrity of the financial system. Here’s what they impact the most.

Risk mitigation

CIP and KYC collectively mitigate financial risks by ensuring the banks know who they are dealing with. Establishing a customer identity accurately and comprehensively at the outset reduces the likelihood of fraud.

CIP program processes are designed to weed out potential threats like identity theft by requiring proof of identity and cross-checking information against various databases. This protects banks from exposure to credit risk, operational risk, and reputational damage that can arise from being associated with financial crime.

Regulatory compliance

Financial institutions are under constant scrutiny to comply with a myriad of regulations designed to uphold the integrity of the global financial system. CIP and KYC are at the heart of these regulatory requirements, ensuring banks perform due diligence on their clients.

By maintaining robust CIP and KYC practices, banks not only adhere to laws and regulations but also demonstrate their commitment to preventing the financial system from being used for unlawful purposes. Regulatory bodies increasingly focus on these areas, and non-compliance can result in hefty fines and sanctions.

Enhancing security

Finally, CIP and KYC are essential for enhancing the overall security within the banking sector. Verifying the authenticity of identity documents and continuously monitoring customer activities means that banks can create a secure environment for all stakeholders.

This security is not just about protecting the bank’s assets; it’s about safeguarding customers’ identities and financial health. In an era where digital identity is as important as a physical one, banks leverage technology like AI-powered solutions to capture, extract, and verify customer data quickly and accurately, further bolstering security measures.

Best Practices for a Stronger CIP KYC Framework

- Adopt a risk-based approach – Apply stricter verification for higher-risk account types or geographies.

- Leverage AI-powered document authentication – Detect tampered or AI-generated IDs with advanced image forensics.

- Integrate sanctions and PEP screening – Ensure onboarding includes immediate watchlist checks.

- Automate audit trails – Maintain secure, exportable records for examiners.

- Continuously test defenses – Run simulated fraud attempts to ensure systems catch synthetic IDs.

Future-Proofing CIP in Banking

The volume of digital account openings is skyrocketing, and fraudsters are adopting generative AI to create near-perfect fake identities. CIP in banking can no longer rely solely on manual checks or legacy systems.

To stay compliant and secure, banks should:

Integrate CIP into an enterprise-wide risk management strategy

Update CIP procedures regularly to align with FinCEN guidance

Train compliance teams on emerging fraud tactics

Invest in adaptable, AI-driven KYC platforms

How Microblink can help

The journey towards meeting compliance constantly evolves, with new regulations and technologies shaping the landscape. Banks must be proactive, not reactive, in their approach to CIP in banking and KYC.

Staying informed about regulatory changes and emerging technologies is crucial for banks to adapt their security measures effectively. Focus on your core business, but be ready to adapt to change at a moment’s notice. You’ll need a reliable partner to do both tasks effectively.

Microblink is at the forefront of providing AI-driven solutions that aid banks in capturing, extracting, and verifying digital identity. Our BlinkID product streamlines the CIP process, ensuring identity document verification is compliant but also user-friendly and secure. For KYC, our technology empowers banks to conduct ongoing, real-time verification with greater accuracy and less friction for the customer. To learn more, get in touch today.