What is a Customer Identification Program (CIP)?

Imagine a world where financial transactions are invisible threads connecting individuals across the globe, with no accountability or traceability. Such a world would be full of money laundering, fraud, and a haven for financial criminals. This is the dystopia that customer identification programs prevent.

Implementing a customer identification program (CIP) allows financial institutions to uncover illicit transactions and ensure every thread leads back to a real person accountable for their financial activity. So, what is CIP, and why is it a cornerstone in the architecture of financial security?

What is a customer identification program?

A customer identification program is a critical component in the financial industry’s arsenal against financial crimes. It’s a policy that requires financial institutions to verify the identities of their customers. The essence of what CIP is can be distilled into its role as a gatekeeper, ensuring only legitimate individuals and entities gain access to financial services, thus safeguarding the economic framework from abuse.

The customer identification program isn’t just a recommendation; it’s cemented in regulations and enforced by regulatory bodies worldwide. These authorities, such as the Financial Crimes Enforcement Network (FinCEN) in the United States, set the standards for CIPs and mandate their implementation to combat other financial crimes. The program’s importance is magnified by financial transactions, which are the lifeblood of banking and various other sectors, from eCommerce to real estate.

In practice, a CIP requires financial institutions to collect personal information like names, addresses, and identification numbers. They must also verify this information against credible documents, databases, or other reliable sources. The process doesn’t just stop at onboarding; continuous monitoring is essential to ensure ongoing compliance and to flag any suspicious activity.

CIP in finance

Navigating the complex landscape of digital currencies and fintech requires a forward-thinking approach to CIP. The decentralized nature of blockchain technologies and cryptocurrencies poses new challenges in verifying customers’ identities.

Traditional methods may not always suffice due to the lack of a centralized authority and the anonymity features inherent in some digital assets. Solutions centering around advanced document verification and cross-referencing data with reliable sources are becoming increasingly vital. These measures ensure compliance with evolving regulations and help construct trust within the digital finance ecosystem.

CIP in banking

Customer identification programs are the cornerstone of modern banking, serving as the first line of defense against financial crimes. Banks rely on CIP to meet anti-money laundering (AML) regulations and to prevent identity theft and fraud.

A thorough CIP process confirms a customer’s identity through reliable documentation and background checks, creating a secure banking environment.

CIP in eCommerce and online platforms

A robust CIP ensures transactions are secure, compliant, and trustworthy in eCommerce and other online platforms. Identity verification during the customer onboarding process helps online retailers and service providers mitigate risks and adhere to regulatory demands.

It’s one of the most important factors to consider for maintaining the security of financial transactions and protecting against unauthorized access to user accounts, ultimately fostering a safer online marketplace for consumers and businesses alike.

What is CIP in KYC?

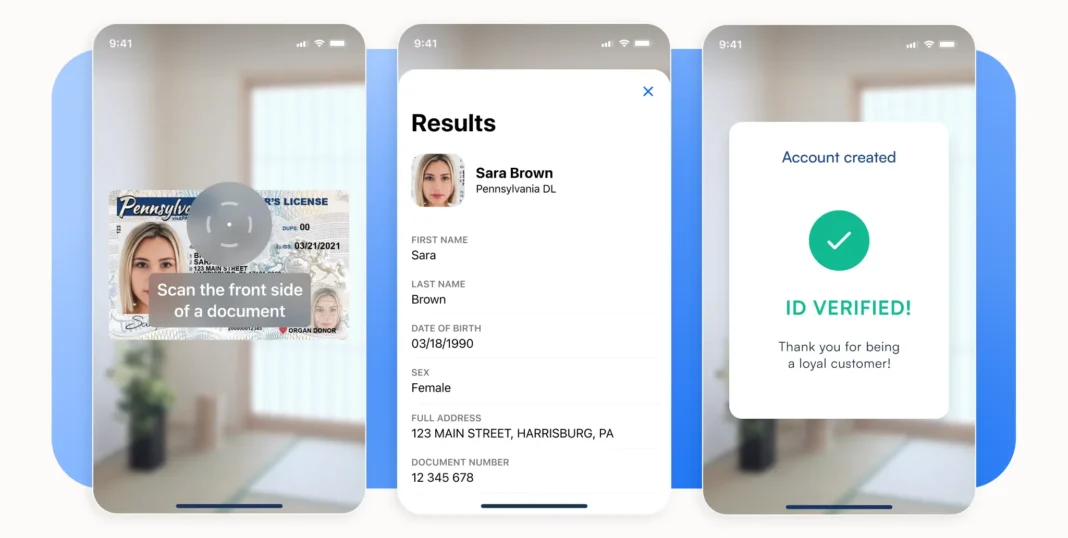

At its core, a customer identification program is a critical component of the know your customer (KYC) guidelines. It mandates that financial institutions and other regulated companies must verify the identity of their clients, ensuring that a bank account is opened in the true customer’s name.

Through CIP, organizations collect information such as name, address, date of birth, and identification number, which is then meticulously verified to confirm the customer’s identity. This KYC ID verification process is not just about compliance; it’s a fundamental practice underpinning the trust relationship between financial services, their customers, and the broader economy.

Who is subject to the CIP rule?

Determining when the KYC process should be performed comes down to the nature of the relationship. Banks and credit unions are often prime targets for financial crimes.

But CIP extends beyond these to include diverse entities in the financial ecosystem. According to FinCEN, any institution that enters into an enforceable agreement with a customer must implement a CIP.

Money service businesses

These are often the first port of call for financial transactions, especially for those without access to traditional banking. They’re obligated to deploy robust identity verification measures to combat financial crimes.

Brokers and dealers

As gatekeepers of the investment world, they must ensure their customers are who they claim to be, leveraging CIP to uphold market integrity.

Insurers

Given the volume of financial transactions they handle, insurers must adhere to CIP rules, validating the identities of policyholders to prevent fraud.

Fintechs

As the vanguard of financial innovation, fintechs are subject to CIP regulations to maintain trust and security in their digital offerings.

Foreign financial institutions

Even institutions beyond our borders must comply with CIP mandates to ensure a level playing field when engaging with US customers.

Customer identification program requirements

CIP verification is the bedrock of many financial regulations. Principally, it stems from KYC standards that compel institutions to implement a rigorous CIP process to identify and verify the identities of their clients.

CIP requirements demand that financial institutions have a documented CIP program in place, one that is tailored to the institution’s size, its customer base, and the potential risks it faces. This means conducting a risk assessment to gauge and assess potential risks associated with each customer.

Customer verification procedures

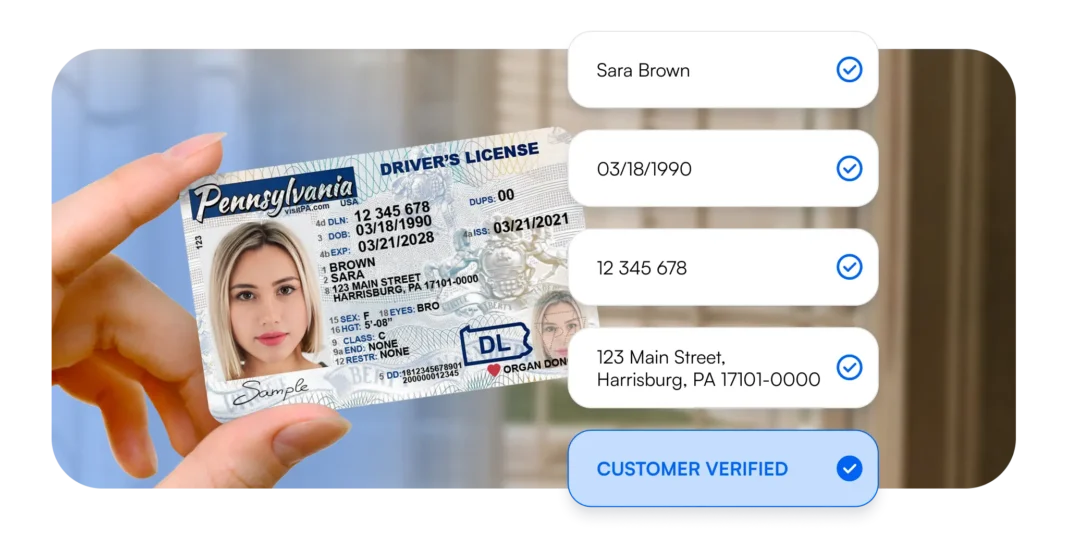

The CIP process isn’t one-size-fits-all. Institutions must use document-based and non-documentary methods to confirm a customer’s identity. Documents such as passports, driver’s licenses, or other government-issued IDs are standard for establishing identity.

Non-documentary methods might include cross-checking information with credit bureaus or public databases. The goal is to achieve assurance that the customer is genuinely who they claim to be.

Recordkeeping requirements

A paper trail—or, these days, a digital one—is essential for compliance. CIP mandates that financial institutions maintain records of the information used to verify a person’s identity.

This could include copies of identification documents or the methods and results of any measures taken to verify identity. These records must be kept for a specified period, typically several years after closing the account.

Ongoing monitoring

CIP isn’t a “set it and forget it” affair. It demands ongoing monitoring to ensure that customer relationships remain above board.

This risk-based approach requires institutions to monitor transactions that don’t fit the pattern of a customer’s usual activity. It’s about staying vigilant, updating customer information, and reassessing risks as relationships evolve.

Best practices for implementing an effective CIP

When creating or refining a CIP program, the ultimate goal is to construct a framework that not only adheres to regulatory standards but also delivers an experience that respects the customer’s time and needs. A thoughtfully implemented CIP program is essential in building trust and ensuring the integrity of financial transactions.

At the heart of an effective CIP program lies the accurate capture of a government-issued identification number, which forms the cornerstone of identity verification. By incorporating such data, businesses establish a reliable point of reference that supports the rest of the customer identification process. This critical step must be handled precisely, as it ties directly to legal compliance and fraud mitigation.

The process of collecting customer information is a delicate balance between thoroughness and efficiency. In this digital age with short attention spans, it’s imperative to streamline customer data acquisition to avoid deterring potential users with cumbersome procedures. An optimized data collection approach enhances customer satisfaction and sets the stage for more effective identity verification.

Customer due diligence is a continuous imperative beyond the initial account setup, encompassing ongoing monitoring to detect and respond to any changes in customer activity that might indicate risk. A proactive stance safeguards the institution and aligns with a commitment to maintaining a secure and trustworthy environment for all customers.

How Microblink can help

Leveraging government-issued identification numbers, optimizing the collection of customer information, and refining identity verification procedures are all a part of building an effective CIP.

With Microblink’s AI-powered technology, companies can not only meet these best practices but also enhance the customer experience, making identity verification seamless and secure. It’s time to assess your CIP processes, stay ahead of regulatory changes, and elevate your customer identification strategy with Microblink’s cutting-edge solutions.

FAQ

-

What is a CIP in finance?

In finance, CIP is a security protocol ensuring financial institutions correctly identify and verify their customers’ identities.

-

What is a CIP in banking terms?

CIP in banking is the process banks use to verify customers’ identities as part of their due diligence and AML strategies.

-

What is a business CIP?

A business CIP refers to the procedures and policies businesses implement to comply with legal mandates for customer identification and verification.