3 Keys Elements of Customer Identification Program for AML

In the fight against financial crimes, anti-money laundering (AML) is a critical defense. AML refers to procedures, laws, and regulations to prevent criminals from disguising illegally obtained funds as legitimate income.

Core to these efforts is the customer identification program (CIP), a vital component in safeguarding the financial system. In this article, we’ll explore the pivotal elements of a customer identification program, ensuring compliance and protecting institutions from complicity in financial misdeeds.

The role of CIP in AML compliance

CIP serves as a foundational element in the arsenal of anti-money laundering procedures deployed by financial institutions. At its core, CIP mandates that financial institutions establish a reasonable belief in the true identity of their customers. This is essential in today’s digital economy, where financial transactions often occur without face-to-face interactions.

CIP is the initial filter in a multi-layered defense system designed to detect and deter money laundering and other financial crimes. By implementing rigorous identification program protocols, financial institutions can significantly reduce the risk of illicit activities, ensuring only legitimate and verified users can access financial services.

Protection against identity theft

CIP isn’t just about safeguarding the financial system but also protecting individuals from identity theft. According to the US Treasury’s recent money laundering risk assessment, criminals often create synthetic identities to defraud financial institutions of significant sums of money.

Requiring stringent verification of identity documents and personal information makes it much more difficult for criminals to misuse someone else’s identity for fraudulent purposes. Plus, this process helps shield consumers from the financial harm and emotional distress often accompanying identity theft.

Enhancement of customer trust

Trust is the currency of the financial sector, and applying the elements of a customer identification program is vital in strengthening this trust. Customers feel more secure knowing their financial institution takes the verification of identities seriously and is committed to preventing financial fraud. This trust translates into greater customer loyalty and confidence in their transactions and personal data security.

Compliance with regulations

CIP isn’t only a best practice—it’s a regulatory requirement. Adhering to CIP protocols ensures financial institutions remain compliant with anti-money laundering regulations.

Non-compliance can lead to significant penalties, legal repercussions, and reputational damage. Beyond that, a well-executed CIP supports filing suspicious activity reports, ensuring questionable transactions are reported to the relevant authorities, contributing to a broader effort to combat financial crime.

Key elements of a customer identification program

A robust customer identity verification program is the bedrock of a financial institution’s efforts to combat financial crimes. The procedures involved apply not just to banking but also to other financial transactions across various sectors.

In alignment with the Bank Secrecy Act, financial institutions, including banks and consumer reporting agencies, implement the elements of a customer identification program as a shield against the infiltration of illicit funds into the financial system.

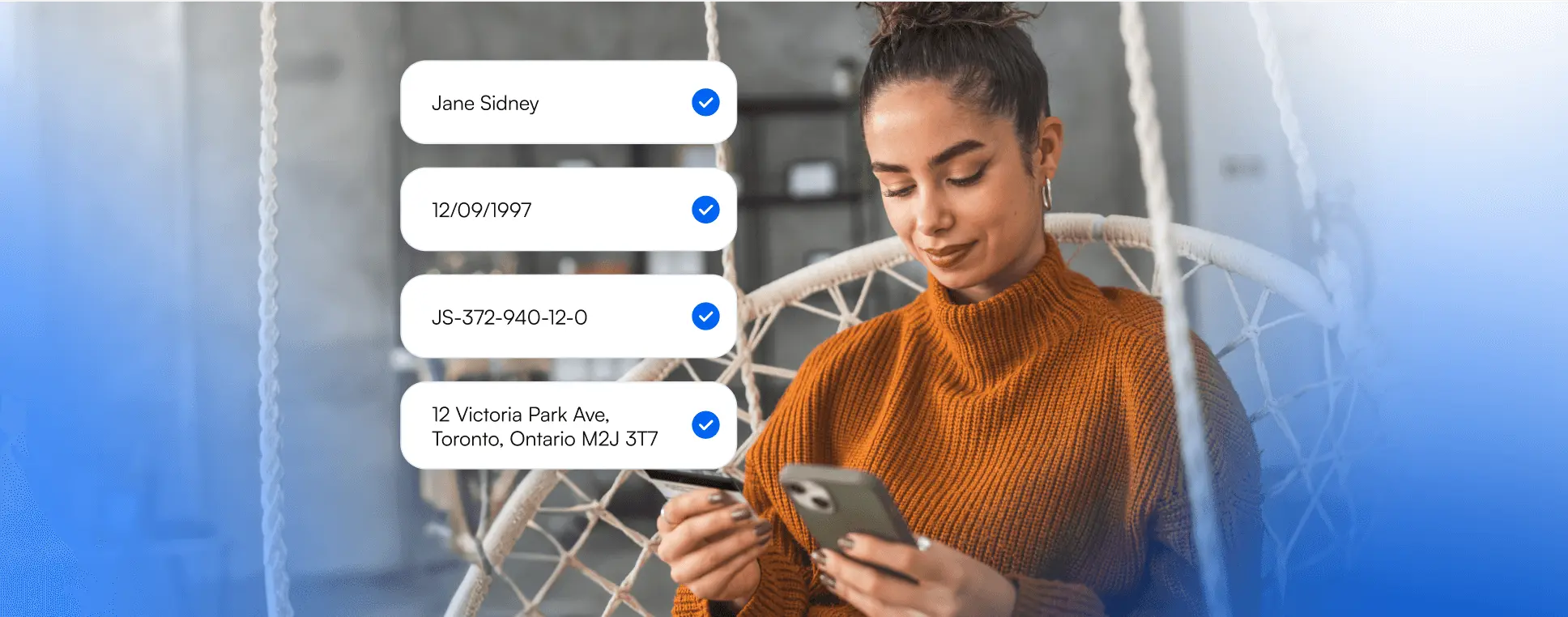

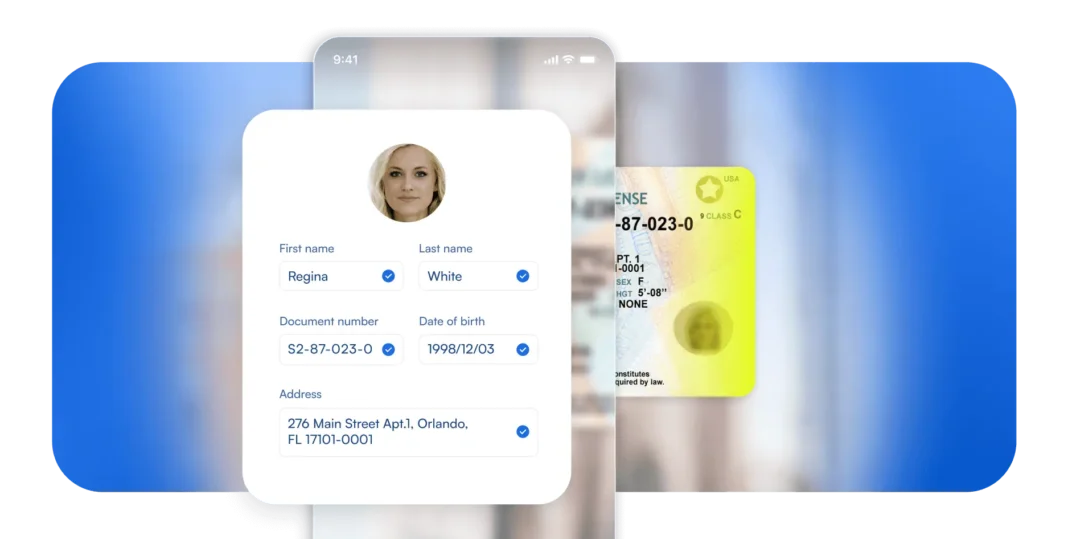

Identification and verification of customers

Understanding the importance of customer due diligence (CDD) is crucial for any financial institution. CDD involves several components that help firms comprehend their customers’ behaviors and manage their associated risks.

These components include collecting identifying information, employing risk-based procedures to verify that information, and establishing internal controls to ensure ongoing compliance.

The role of CDD extends beyond mere compliance. It’s a strategic component that offers in-depth insights into the nature of customer transactions, helping institutions understand relevant risks. This understanding is pivotal for asset tracking and protecting the financial system’s integrity.

Importance of thorough CDD in preventing money laundering

Inadequate CDD can lead to dire consequences. From hefty fines to legal repercussions, financial institutions face severe outcomes when they fail to perform due diligence. Beyond the legal implications, reputational damage can be even more detrimental, causing long-lasting harm to an institution’s trustworthiness.

Steps involved in CDD

CDD involves meticulous methods and technologies to verify customer identities. This includes checking customer information against databases, employing biometric verification, and using solutions like automated document scanning, which streamline the process through AI-enabled identity document verification.

Understanding a customer’s industry and business model is essential to gauge their potential risks. Moreover, continuous monitoring of accounts is required to detect anomalies or behavioral changes that may signal fraudulent activities.

Risk assessment

Risk assessment is a cornerstone of effective AML compliance, helping institutions allocate resources effectively. It’s about identifying the potential for harm and taking steps to mitigate it.

High-risk customers

Certain industries and customer profiles are typically perceived as high-risk. These might include politically exposed persons or businesses operating in regions known for high levels of corruption.

The penalties for skirting regulations for these clients can be severe. A recent case shows a former bank president who attempted to sidestep anti-money laundering processes faces up to 10 years in prison for assisting high-risk clients in fraudulent schemes.

Medium-risk customers

Customers categorized as medium-risk may involve less obvious risks. These might include those in other financial institutions or businesses with large cash transactions.

Low-risk customers

Low-risk customers often present a minimal risk profile due to their stable financial history or transparent business activities. Despite their lower risk status, they still require due diligence.

Implementing a risk-based approach in CIP

Adapting due diligence procedures based on identified risk levels is imperative. For example, enhanced due diligence might be necessary for high-risk customers. Ongoing assessments are crucial to adapt to evolving risks.

Ongoing monitoring

A CIP isn’t static. It requires periodic reviews and updates to remain effective, ensuring internal controls evolve with changing threat landscapes.

Monitoring tools and strategies are crucial for identifying and investigating suspicious behaviors. A proactive approach can prevent financial crimes before they occur.

Importance of innovation in CIP development

Incorporating innovative tools and techniques is vital for accurate and reliable customer identity verification. Automation plays a significant role in streamlining the verification process, while AI and machine learning are pivotal in identifying suspicious patterns proactively.

Leveraging customer identity verification software that uses these technologies can ensure your CIPs are compliant, efficient, and effective in preventing money laundering and other financial crimes.

The future of customer identification programs

Combining customer due diligence, risk assessment, and technology automation is vital to forming a CIP. These elements are fundamental for financial institutions to meet and exceed regulatory demands, laying a groundwork of integrity with clientele.

A meticulously crafted CIP stands at the heart of AML compliance, with accurate customer identity verification procedures acting as a primary defense against financial threats.

How Microblink can help

To keep pace with evolving risks and regulatory demands, financial institutions must regularly update and improve their CIPs. Microblink’s cutting-edge technology supports this imperative, offering tools like customer identity verification APIs for swift and precise identity document verification. This proactive, document-centric verification approach is key in slashing fraud rates.

Continuous adaptation of CIP strategies is crucial as threats and regulations change. Microblink’s dedication to innovation ensures clients consistently benefit from the most advanced technology for their CIP requirements.