KYC Checklist: For Top Banks and Financial Institutions

The KYC (short for know your customer) process is increasingly important for banks and financial institutions. Besides protecting against money laundering, financial crimes, and other criminal activities, KYC is essential for banks that protect their customers’ identities and financial well-being.

This post will unpack the importance of KYC and explore how AI-powered technology can enhance the KYC checklist for banks. Smart tech can streamline identity verification, making it faster, more accurate, and less susceptible to fraud. We’ll also explore how banks can use these technologies to not only meet compliance standards but also improve customer experience.

The significance of KYC for banks and financial institutions

In the context of heightened global scrutiny and the evolving landscape of financial crimes, KYC practices are not just regulatory formalities but are foundational to the integrity of financial institutions.

KYC procedures serve as the first line of defense against money laundering, a critical step in identifying potential financial criminals, and a means to combat various financial crimes effectively.

Implementing robust KYC protocols is arguably the best way for banks and other financial entities to detect suspicious activities early, disrupt the flow of illicit funds, and contribute to broader anti-money laundering efforts.

Regulatory requirements

The regulatory requirements for KYC are anchored by global standards set forth by entities such as the Financial Action Task Force (FATF), which provides international norms and guidelines to combat money laundering and terrorist financing.

These global standards require financial institutions to perform due diligence on their customers to better understand their financial behaviors and risks.

Additionally, national regulations, which can vary significantly by country, reinforce these standards with specific legal obligations, outlining customer identification, verification, and ongoing monitoring processes.

Fraud prevention and risk management

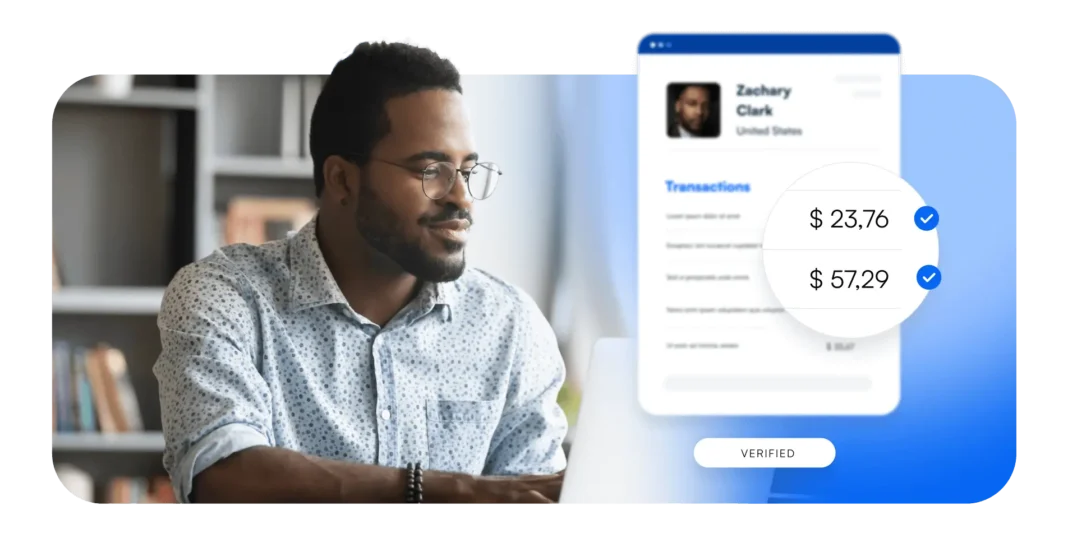

Effective KYC is synonymous with fraud prevention and risk management in the banking sector. Financial institutions can identify irregular transaction patterns and assess risk profiles by accurately capturing, extracting, and verifying customer data, taking swift action when red flags arise.

Favoring a more proactive approach such as this not only protects the banks’ assets but also safeguards the financial system at large from being exploited for fraudulent purposes. Companies that adopt AI-powered solutions for identity document verification, like BlinkID, are at the forefront, reducing fraud by more than 50% through advanced technology that uncovers the authenticity of documents.

Building trust with customers

Trust is the currency of the banking industry, and KYC is a pivotal tool in building and maintaining this trust. It reassures customers that their chosen financial institution values security and is committed to protecting their assets from financial criminals.

Furthermore, banks can enhance customer relationships by offering seamless and user-friendly KYC processes, ensuring compliance and convenience. This balance is crucial, as it fosters a sense of confidence and loyalty among customers, cementing the institution’s reputation as a trusted and secure place to manage financial affairs.

Compliance requires careful preparation

Checklists are essential for managing KYC compliance, serving as navigational beacons for employees across financial institutions. From frontline staff to senior compliance officers, a well-structured checklist provides a clear outline of necessary steps, helping to ensure no critical element is overlooked.

At the initial compliance stage, checklists assist in standardizing procedures so that all customer profiles are evaluated consistently. They prove equally invaluable in ongoing compliance efforts, providing a framework for a regular risk assessment and review process.

Even at the individual level, incorporating checklists can help efficiently manage responsibilities, stay aligned with regulatory expectations, and mitigate non-compliance risk.

Common elements of the KYC checklist

A robust KYC checklist is the backbone of an effective compliance program. It typically includes elements critical to customer due diligence, such as verifying the identity of new clients, performing a detailed customer due diligence process, and, when necessary, conducting enhanced due diligence on higher-risk customers.

The customer checklist is a living document that supports the ongoing process of maintaining up-to-date customer information throughout the customer onboarding process and beyond. It helps to ensure that ongoing monitoring is not just a policy but a practice, facilitating the early detection of any discrepancies or suspicious activities.

Customer identification program (CIP)

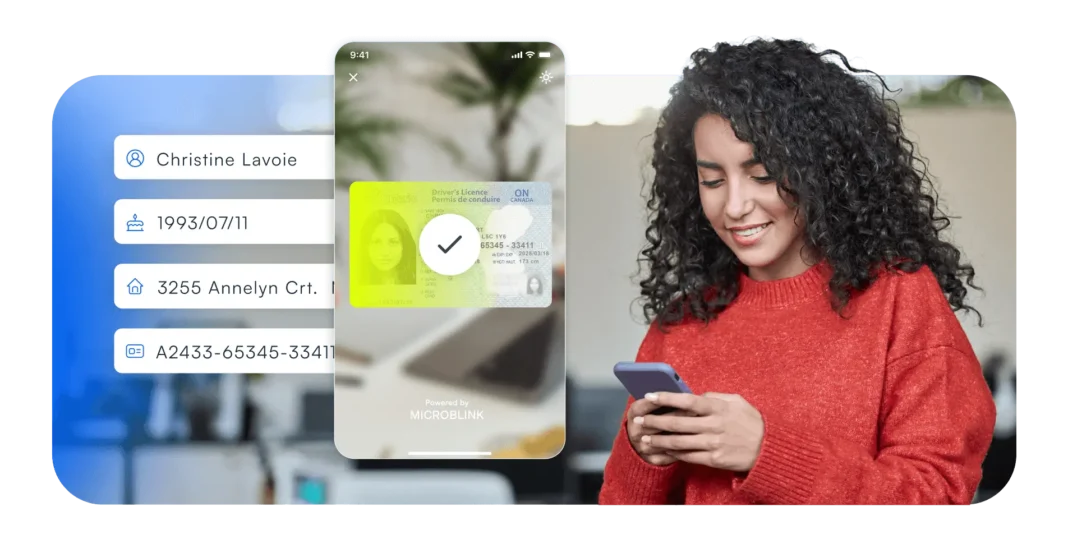

Verification of identity documents is a cornerstone of the CIP. It involves examining reliable, independent source documents to establish a customer’s identity. Tools like BlinkID enhance this step by enabling AI-powered document scanning and verification, streamlining the process while maintaining accuracy and security.

Enhanced due diligence is especially crucial for high-risk customers. This involves additional investigative measures to understand the customer’s background, financial profile, and the nature of the risk they present. Ensuring thorough scrutiny helps in mitigating potential compliance issues.

Customer due diligence (CDD)

Understanding the nature of the customer’s activities is fundamental to CDD. This insight allows financial institutions to anticipate transaction patterns and identify when activities deviate from the norm, which could indicate potential risks or illicit behavior.

Assessing the risk associated with the customer helps categorize customers based on the required level of due diligence. This risk-based approach is vital for allocating resources effectively and ensuring that higher-risk customers undergo more intensive scrutiny.

Ongoing monitoring

Regular updates of customer information are crucial to maintaining the accuracy of the customer profiles. Changes in customer circumstances or business activities can alter their risk profile, necessitating continuous updates for effective risk management.

Monitoring transactions for suspicious activity is a proactive measure to detect and prevent illicit activities. Financial institutions can quickly identify and investigate anomalies by observing transaction patterns and comparing them to expected behavior, thereby safeguarding against financial crimes.

Who can benefit from a KYC document checklist?

KYC documents are essential for maintaining regulatory compliance within the financial services industry. A KYC document checklist is a critical tool for verifying a customer’s identity, ensuring that businesses operate within legal frameworks while mitigating fraud and money laundering risks.

Accountants

Accountants can significantly benefit from a KYC document checklist. It streamlines their due diligence processes, ensuring their financial record-keeping is accurate and compliant with the law. Having a clear set of KYC documents can be a game-changer for accountants looking to efficiently verify the identities of their clients, establish the legitimacy of their sources of funds, and maintain integrity in financial reporting.

Financial service providers

Financial services companies, which form the backbone of the financial services industry, are perhaps the most in need of comprehensive KYC document checklists.

As gatekeepers to financial transactions and services, they must ensure that the identity verification processes for new and existing customers are thorough and foolproof. A well-structured KYC checklist helps these providers prevent identity theft, financial fraud, and other illicit activities that could compromise their operations and customer trust.

Consider automation

In the modern digital landscape, automation stands out as a beacon of efficiency, particularly when the precision of ML/AI bolsters it. Automating KYC processes can lead to a multitude of benefits:

- Enhanced accuracy in identity verification

- Streamlined onboarding experiences for customers

- Reduced manual errors and operational costs

- Improved compliance with ever-evolving regulations

How Microblink can help

Microblink stands out with AI-powered solutions that capture, extract, and verify identity documents. Its flagship product, BlinkID, is designed to automate the KYC process with impeccable precision.

Businesses can transform their KYC checklist into a dynamic, AI-driven workflow, ensuring that financial services companies, accountants, and any entity in the financial services industry can securely and efficiently validate a customer’s identity.

With Microblink, the promise of AI-enabled KYC goes beyond just meeting compliance standards—it enhances the overall customer journey and builds trust through robust, seamless user experiences.