Customer Identity Verification in Banking: What It Is and Why It Matters

The rapid rise of online and mobile banking has reshaped how financial institutions engage with customers. By 2026, digital banking users in the U.S. are projected to reach nearly 48 million, up from 33 million in 2023. But as adoption soars, so does the threat of online banking fraud.

For product managers designing onboarding flows for digital banking platforms, customer identity verification sits at the crossroads of trust, compliance, and user experience. The challenge: protect your institution and your customers without creating friction that drives users away.

In this guide, we’ll explore what online banking identity verification is, how it supports KYC (Know Your Customer) and AML (Anti-Money Laundering) compliance, and how to build seamless, secure onboarding experiences that earn user trust from day one.

What Is Online Banking Identity Verification?

Identity verification in online banking apps is the process of confirming that a new or returning user is who they claim to be. It’s the foundation of both customer trust and regulatory compliance.

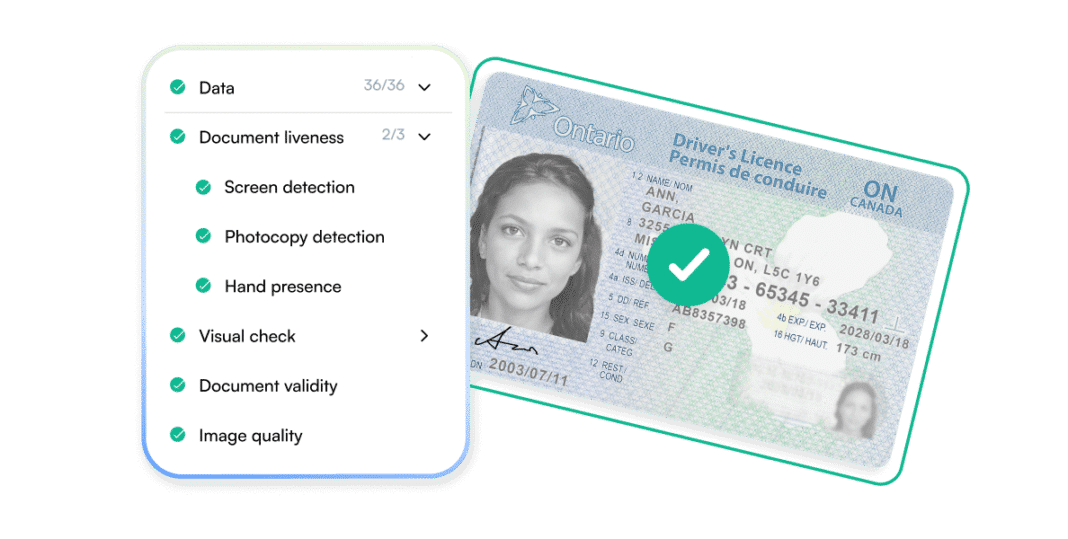

Traditionally, this meant in-person checks, such as reviewing passports, driver’s licenses, or utility bills. Today, leading banks use AI-powered digital verification to analyze ID documents, match biometrics, and detect fraud in seconds.

The goal remains the same: ensure the person opening or accessing an account is legitimate. What’s changed is the speed, sophistication, and automation now possible through technology.

Manual vs. Automated Verification

Manual verification used to define the banking world. Customers submitted physical documents, waited for human review, and often faced multi-day delays before gaining account access.

Even as banks digitized, many adopted a “hybrid” approach, allowing users to upload ID photos online but still requiring back-office staff to verify them manually. While this improved convenience, it didn’t solve the friction problem.

Modern, automated verification systems powered by computer vision, machine learning, and OCR (optical character recognition) now enable real-time checks. They extract and cross-validate ID data, match facial biometrics, and flag inconsistencies automatically.

The result:

- Faster onboarding and access to accounts

- Reduced operational costs and manual workload

- Lower fraud risk and compliance errors

For online banking platforms, automation isn’t just about efficiency, it’s a competitive differentiator that enhances trust and user satisfaction.

Why customer identity verification is crucial in banking

A recent study revealed merchants in the United States suffered losses of 3.75 U.S. dollars for every dollar of online fraud, which has ripple effects across the global banking sector. But why such a significant multiplier effect for every fraud dollar?

The answer lies in the aftermath of the fraud. For each fraudulent dollar, there are costly labor and investigations, fees racked up during the applications, underwriting, and processing stages, and not to mention the legal fees and external recovery expenses. some challenges include:

1. Regulatory Compliance

Online banks must meet stringent KYC and AML obligations to prevent money laundering, terrorist financing, and synthetic identity fraud. FATF guidelines emphasize robust verification and ongoing monitoring to maintain compliance.

2. Fraud Detection

As fraud tactics evolve—using deepfakes, AI-generated IDs, and stolen credentials—traditional verification systems struggle to keep up. Automated verification with document authenticity checks and liveness detection helps spot anomalies instantly.

3. Customer Trust and Reputation

Security lapses can destroy years of brand equity. Customers expect their digital bank to safeguard both their identity and their time. A seamless, secure verification process reassures users that their data is protected and keeps them loyal.

The Building Blocks of Identity Verification

Modern identity verification in online banking apps combines several layers of technology to confirm identity, assess risk, and ensure compliance.

1. Document Verification

Government-issued IDs (passports, national IDs, driver’s licenses) are scanned and authenticated using AI-driven software. The system extracts data, validates its format, and compares it to known templates and databases.

2. Biometric Verification

Facial recognition and liveness detection add another layer of protection, confirming that the user is present and not using a spoofed or stolen image.

3. Multi-Factor Authentication (MFA)

MFA adds redundancy by combining “something you know” (like a password) with “something you have” (a one-time code) or “something you are” (a biometric).

4. Risk-Based Verification

Leading platforms now integrate behavioral analytics and device intelligence to dynamically adjust verification levels. A trusted returning user may pass with lighter friction, while a suspicious session triggers enhanced checks.

Balancing Security with User Experience

One of the hardest challenges for product managers is avoiding the friction trap: adding so many layers of verification that legitimate customers abandon onboarding.

The best approach is risk-based orchestration:

- Use adaptive verification that scales security according to transaction risk.

- Design intuitive capture flows that guide users to submit high-quality ID photos.

- Integrate verification natively into the app to avoid redirects or context switching.

When verification feels like part of the brand experience, banks gain both compliance confidence and customer satisfaction.

What are the Differences Between a Customer Verification API and SDK?

In customer identity verification, you might notice two terms keep popping up: API and SDK. Their roles in enhancing applications, especially customer verification, are paramount, but understanding their unique characteristics is crucial for an optimal integration experience.

An API, short for application programming interface, is the silent connector for software components, making real-time data sharing possible. However, its cloud-based nature means it leans heavily on a constant internet connection. There’s an alternative with the self-hosted API, offering more control at the expense of direct management and maintenance.

Meanwhile, the SDK, or software development kit, is a comprehensive developer toolkit. Designed for deep integration into apps, it offers many features, including the vital ability to operate offline.

Integration with Other Banking Systems

Identity verification doesn’t operate in isolation. To maximize effectiveness, it should connect seamlessly to:

- Transaction monitoring systems to flag risky behavior after onboarding.

- Fraud prevention tools to correlate identity data with behavioral or device signals.

- Risk scoring engines to continuously evaluate account integrity.

APIs and SDKs are the backbone of this ecosystem. They allow real-time data exchange between verification systems and broader banking platforms, ensuring consistency, auditability, and speed.

Microblink’s BlinkID and BlinkID Verify exemplify this interoperability. They combine real-time document scanning, biometric validation, and data matching in a developer-friendly platform that integrates with both cloud and on-prem environments.

How to Automate Identity Verification Processes with Microblink

Gone are the days when verifying a customer’s identity was a cumbersome, manual process. Employing customer identity verification software is a huge step in the right direction.

With Microblink’s AI-powered document and biometric verification, flexible SDKs and APIs, and proven accuracy at scale, banks can onboard users confidently while maintaining compliance and efficiency.