Best Digital Onboarding Solutions for Banks: Features, Comparisons, and Buyer’s Guide

Digital onboarding is now mission-critical for banks and credit unions aiming to deliver secure, compliant, and seamless customer journeys—completely online. Whether your focus is reducing abandonment rates, accelerating time-to-card, or improving post-opening engagement, choosing the right platform is essential to success. This guide breaks down the leading digital onboarding solutions, comparing their strengths, core features, and best-fit use cases to help banks navigate their options with confidence.

Digital Onboarding Solutions for Banks: Quick Comparison

| Vendor | Primary Strength | Core Features | Ideal For | Pricing |

| Microblink | Best-in-class ID Verification (IDV) | – Real-time document capture- Biometric/liveness checks- Global eKYC support- Mobile/web SDKs | Banks needing accurate, flexible IDV as part of onboarding | Quote-based; usage-driven |

| Entrust | Secure digital account opening & card issuance | – Biometric IDV- No-code workflow builder- Instant digital/physical credentialing | Banks prioritizing security, speed, and credential delivery | Enterprise; quote-based |

| Salesforce FSC | CRM-centric onboarding orchestration | – No/low-code workflows- Integrated e-sign & disclosures- 3rd-party IDV support | Institutions using Salesforce CRM with onboarding needs | Per-user license + add-ons |

| Digital Onboarding | Post-opening engagement & activation | – Campaign automation- Retention analytics- Omnichannel messaging | Teams focused on activation, cross-sell, and customer lifecycle | Enterprise subscription; quote |

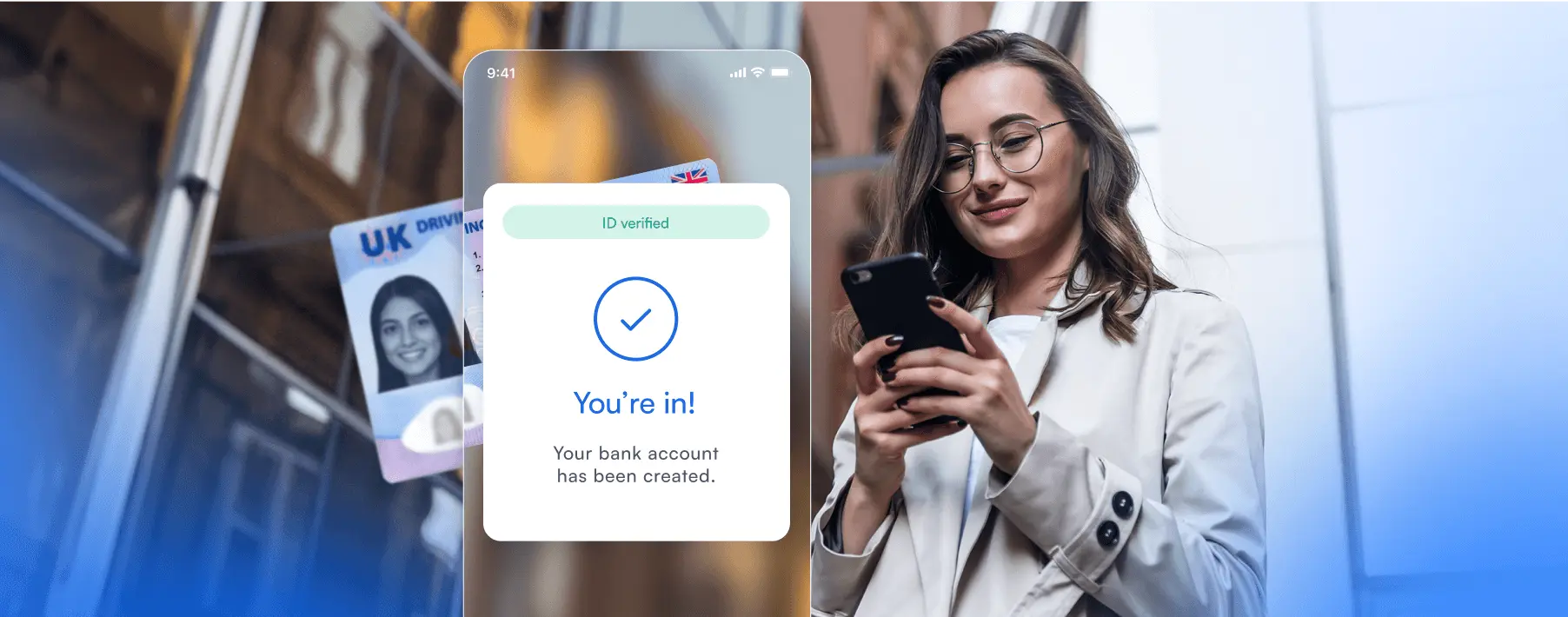

1. Microblink

Best for fast, accurate ID verification in digital account onboarding.

Microblink offers a high-performance identity verification engine that powers seamless digital account opening with real-time document scanning, on-device liveness detection, and global ID coverage. Its flagship product, BlinkID, is trusted by leading banks and fintechs to streamline onboarding and prevent fraud without sacrificing UX.

Key Features

- AI-powered scanning for passports, driver’s licenses, and national IDs

- Adaptive image capture for high-quality scans, even on low-end devices

- On-device biometric verification and liveness checks

- Support for 140+ countries with global eKYC capabilities

- Lightweight SDKs for iOS, Android, and web platforms

Pricing

Custom, quote-based pricing based on volume and features.

Pros

- High accuracy and speed reduce manual reviews

- Privacy-first with on-device data processing

- Rapid integration via developer-friendly SDKs

- Proven results, e.g., 40% uplift in ID capture rates for Binance

Cons

- Platform launched 2025, newer orchestration on the market compared to legacy technology

- No manual reviewers

- Not suitable for IAM use cases

Use Cases

- Instant ID verification for retail account opening

- Secure onboarding for remote loan origination

- Multi-country compliance for cross-border banking

2. Entrust

Best for secure onboarding with instant card issuance.

Entrust delivers a comprehensive digital onboarding experience combining biometric identity proofing, no-code workflow configuration, and secure credential issuance. With advanced fraud detection and robust compliance features, Entrust is suited for banks that value security and speed at scale.

Key Features

- Biometric identity verification with real-time document proofing

- Drag-and-drop no-code workflow builder

- Instant digital and physical card issuance

- Device intelligence and eKYC integration

- Detailed audit logs and compliance reporting

Pricing

Enterprise quote-based pricing that scales with usage and selected modules.

Pros

- Strong anti-fraud and identity assurance capabilities

- Instant credentialing improves customer activation rates

- Business-friendly no-code tools for fast deployment

Cons

- Higher cost may not suit smaller institutions

- Integration with legacy systems may require additional effort

Use Cases

- Retail and business account opening

- High-risk account fraud prevention

- AML-compliant digital onboarding

3. Salesforce Financial Services Cloud (FSC)

Best for institutions seeking CRM-integrated onboarding workflows.

Salesforce FSC empowers banks to manage digital onboarding directly within their CRM using low-code tools and third-party integrations. With a unified customer view, banks can orchestrate seamless onboarding journeys, track engagement, and automate compliance touchpoints across teams.

Key Features

- No/low-code workflow creation for digital onboarding

- Integrated e-signatures, consent collection, and disclosures

- Prebuilt connectors for Marketing Cloud, MuleSoft, and Slack

- Support for third-party IDV and fraud prevention tools

- Unified Customer 360 view across sales, service, and onboarding

Pricing

Per-user licensing (based on FSC edition) plus optional module add-ons.

Pros

- Full visibility across the customer lifecycle

- Flexible and scalable onboarding workflows

- Deep Salesforce ecosystem integration

Cons

- Requires existing Salesforce CRM investment

- May be cost-prohibitive or complex for smaller banks

Use Cases

- CRM-native onboarding for retail and business banking

- Centralized regulatory compliance tracking

- Automated upsell and cross-sell during onboarding

4. Digital Onboarding

Best for driving activation, cross-sell, and retention post-account opening.

Digital Onboarding focuses on engagement beyond day one. Designed for banks and credit unions, it provides turnkey campaign tools and behavioral analytics to increase product adoption, reduce churn, and build lasting relationships with new customers.

Key Features

- Ready-to-use campaign templates with customization options

- Automated engagement journeys with real-time analytics

- Easy data import via API, SFTP, or CSV

- Omnichannel outreach across email, SMS, and digital banking portals

Pricing

Enterprise subscription pricing, tailored to usage and feature set.

Pros

- Fast, lightweight deployment with no infrastructure requirements

- Measurable results on customer retention and product adoption

- Low technical overhead, ideal for smaller teams

Cons

- Not a full-stack onboarding or ID verification platform

- Integration with core systems required for full functionality

Use Cases

- Activation campaigns post-account opening

- Automated cross-sell/upsell based on user behavior

- Churn reduction and lifecycle engagement

Frequently Asked Questions

What is digital onboarding for banks?

Digital onboarding is the process of verifying a customer’s identity and opening financial accounts online, using secure technology to meet regulatory, fraud prevention, and user experience standards.

How do digital onboarding platforms reduce fraud?

These solutions use real-time document verification, biometric liveness detection, AI-driven risk scoring, and device intelligence to prevent identity fraud and synthetic accounts.

What compliance standards do these platforms support?

Most leading platforms support major regulatory standards, including KYC, AML, GDPR, and region-specific frameworks like eIDAS or PSD2.

How long does implementation take?

Implementation times vary but many platforms offer SDKs, APIs, and no-code tools that allow banks to go live in weeks rather than months—depending on integration complexity.

Can these platforms integrate with our core banking or CRM systems?

Yes. Most vendors offer robust APIs, SDKs, and prebuilt connectors for common systems including core banking platforms, CRM suites, and compliance engines.