How Much Does KYC Cost?

KYC, also known as know your customer, is a critical process for financial institutions tasked with confirming the identities of their customers, which helps prevent financial crimes like money laundering and identity theft.

The external costs associated with KYC compliance are often significant, encompassing several financial and operational domains. While multibillion-dollar corporations invest heavily in compliance, many smaller financial institutions simply don’t have the resources.

The good news is that the most forward-thinking companies are leveraging automated solutions and new technology to keep costs down without getting in the way of regulations. But are these methods any good?

In this post, we’ll dive into the different factors that make up compliance costs and what contributes to them. We’ll also share actionable insights on reducing these expenses without compromising on due diligence or the quality of customer service.

Average cost of KYC compliance

These include the tools and technologies used to verify customer identity and the operational procedures that underpin customer due diligence. But in addition to that, some factors compound these costs.

So, focusing on finding where most of your spending is going and sealing up the cracks is crucial. Let’s start with the most immediately apparent source of financial frustration.

Financial costs

For financial institutions, the backbone of KYC compliance lies in robust identity verification tools and compliance software. These systems are engineered to meticulously screen and validate customer information against various databases and watchlists.

The costs associated with such technology can be significant, particularly when considering the advanced software needed to accurately analyze and store vast amounts of data.

Compliance software, which encompasses transaction monitoring systems, customer risk rating, and reporting tools, represents a substantial portion of the technology investment required to meet stringent regulatory requirements.

Operational costs

On the operational front, staff training and salaries constitute a major expenditure for financial institutions. Ensuring employees are well-versed in compliance procedures demands regular training sessions, which come with their own costs. Additionally, the salaries of compliance officers and related staff reflect their specialized skills and the critical nature of their roles in maintaining regulatory adherence.

Administrative expenses add another layer to operational costs. These can include the cost of manual document checks when automated systems flag discrepancies and the maintenance of secure document storage facilities.

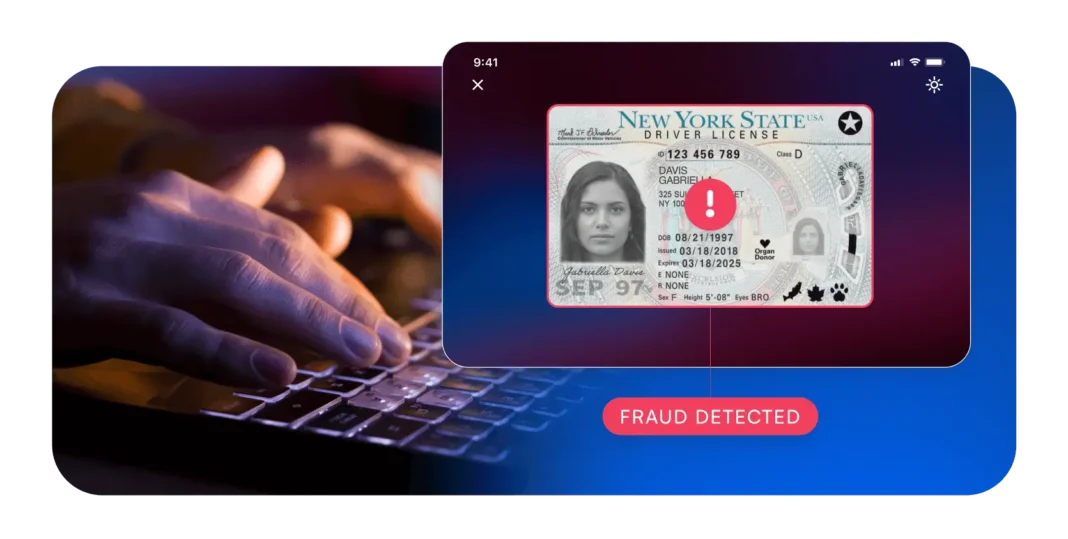

One thing to keep in mind is that the trend leans toward automation when it comes to the choice between automated and manual systems for KYC processes. Automated solutions offer increased efficiency and accuracy and can reduce the likelihood of human error.

However, the initial setup for such systems can be costly, requiring ongoing maintenance and updates. Despite this, the investment in automated systems can ultimately lead to cost savings over time, as they handle higher volumes of verifications with fewer resources.

Regulatory costs

Costs and penalties for non-compliance can be astronomical, sometimes reaching hundreds of millions of dollars for serious infringements. Take this bank, for example, which was fined $400 million for failing to establish an effective risk management framework and not complying with KYC regulations.

Financial institutions invest heavily in compliance to avoid these penalties, which can far exceed the cost of implementing proactive compliance measures.

What contributes to these costs?

Between financial, operational, and regulatory costs, it is pretty clear that KYC compliance can be an expensive venture. But plenty of other factors contribute to these costs even more, making an already costly venture seem daunting.

Industry-specific regulations

The financial sector is governed by various industry-specific regulations designed to combat financial crime. These regulations require a rigorous KYC process to prevent anti-money laundering and financial fraud.

Each industry, whether banking, insurance, or investment, faces its own compliance rules, which may vary in complexity and stringency. Adhering to these regulations requires financial institutions to deploy comprehensive systems and procedures that can be quite costly.

Geographic location and jurisdictional requirements

The geographic location of a financial institution and the legal requirements it must adhere to can significantly impact the cost of KYC compliance. Different countries have different laws and standards for preventing financial crime, meaning a business operating in multiple jurisdictions must navigate a complex web of compliance requirements.

Operating on a global scale can lead to increased legal fees, the need for localized compliance teams, and the implementation of varied onboarding processes to satisfy each jurisdiction’s demands.

Staff salaries

KYC compliance staff are on the front lines of defending against financial fraud. As such, their expertise comes at a cost.

Salaries for compliance professionals reflect the high level of responsibility and specialized knowledge required to navigate the regulatory landscape. Furthermore, ongoing training to update staff on the latest regulations adds to the salary bill.

Fines

Non-compliance can result in hefty fines, which can dwarf the cost of maintaining compliance. Regulatory bodies have been known to impose severe penalties on institutions that fail to perform KYC checks adequately or miss critical risk factors.

These fines are a considerable expense and a clear driver for financial institutions to invest in effective KYC processes to avoid such financial repercussions.

Tools

The tools required for effective KYC, such as identity document verification platforms and biometric authentication technologies, represent a significant investment. These tools must be precise, reliable, scalable, and adaptable to evolving compliance requirements.

Investing in state-of-the-art KYC software is essential for institutions to efficiently manage the onboarding process and maintain high levels of accuracy.

Reputational harm

Beyond financial penalties, the reputational harm from compliance failures is a significant concern. The damage to a brand’s trustworthiness and integrity can lead to customer attrition and difficulty attracting new business.

The cost of repairing a tarnished reputation can be extensive—from public relations campaigns to revamped compliance protocols to regain public confidence. It’s best to keep your reputation intact from the start.

Business size and customer base

The size of a business and the breadth of its customer base also factor into the cost of KYC compliance. Larger institutions with more customers will naturally incur higher compliance costs due to the required KYC verification volume. Conversely, smaller businesses may face relatively lower costs but must still invest in robust KYC processes to remain compliant, regardless of their customer base size.

How to reduce KYC costs

By now, you probably think KYC compliance is too expensive to even consider. But it isn’t optional—it is a necessity. So, how do you bite the bullet and do what needs to be done without running up a massive bill?

Automated KYC

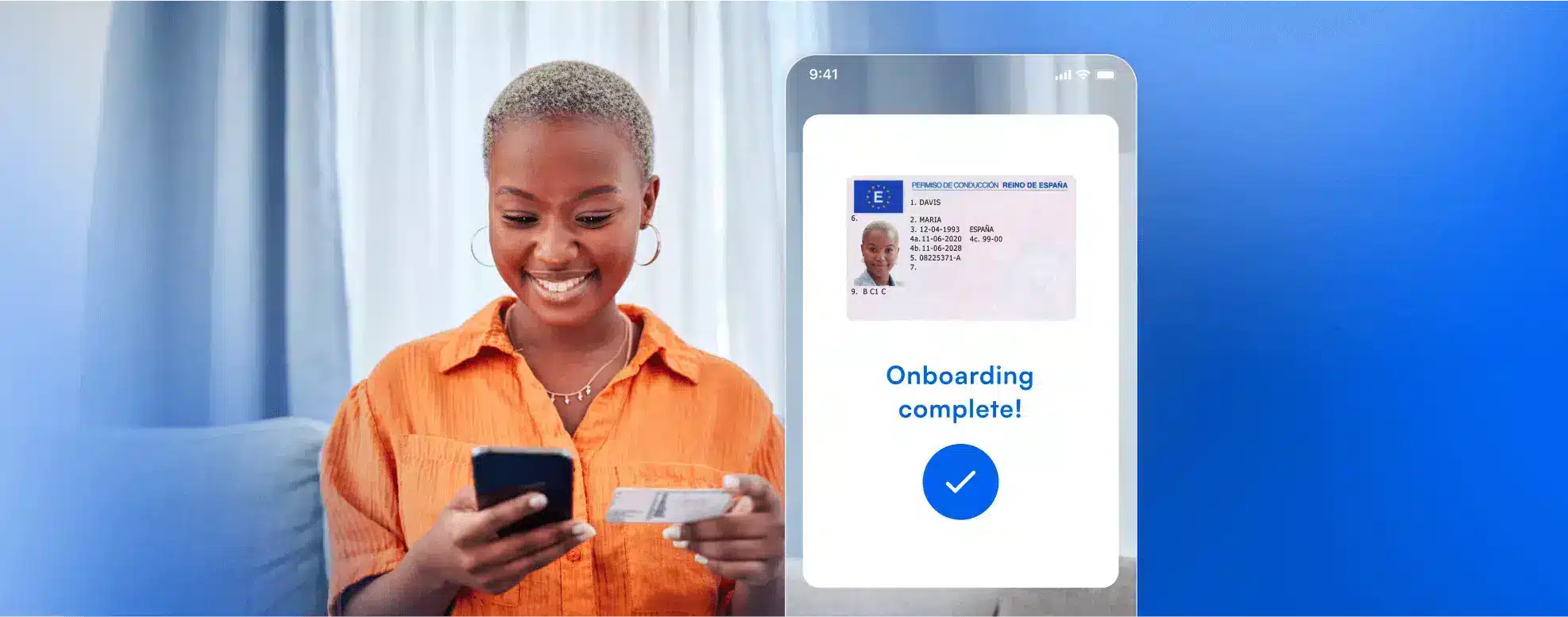

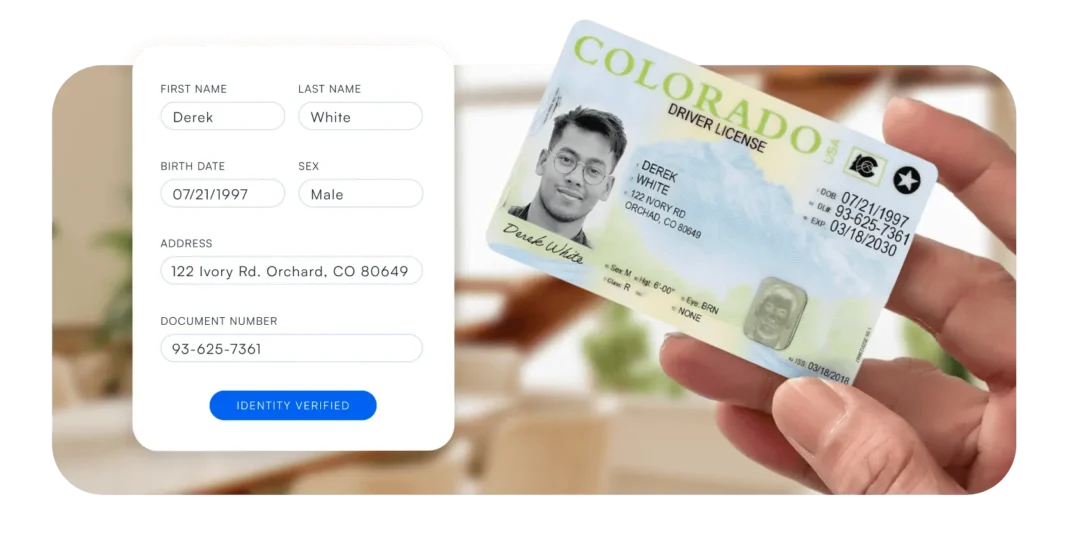

To mitigate soaring KYC costs, automation stands out as the most obvious play. You can significantly reduce the time and labor associated with manual KYC tasks by deploying automated KYC systems.

Since these systems excel in swiftly processing KYC data, they give you a leg up on ensuring compliance with KYC regulations while minimizing human error. For example, automated verification of identity documents streamlines the data extraction process, leading to quick and accurate customer validation.

Leverage third-party software and solutions

Another term that gets thrown around when discussing saving money is outsourcing. However, outsourcing can be a double-edged sword, especially regarding compliance.

On the one hand, third-party KYC solutions offer specialized expertise, often with advanced technology that might be prohibitively expensive to develop in-house. This can lead to enhanced accuracy in document verification and adherence to KYC protocols.

On the other hand, relying on external providers can introduce concerns about data security and control. That’s why selecting a reputable KYC service provider that demonstrates robust security measures and a track record of regulatory compliance is crucial.

Process improvements

Streamlining onboarding procedures is essential for a cost-effective KYC strategy. By refining internal systems and removing unnecessary steps, businesses can accelerate the onboarding process, improving the customer experience while ensuring compliance.

When you improve your processes, you prevent bottlenecks, reduce administrative burdens, and curtail costs associated with lengthy onboarding.

While each of these items might not be much on their own, all of this adds up to be a pretty sizable chunk of savings. To make it even more attractive, you might reap the benefits of improved processes with just a little bit of investigation into how you currently do things—it is not a daunting task.

Monitoring

Continuous monitoring is vital for maintaining KYC compliance and managing risks. Upgrading internal systems for real-time data analysis can preempt potential compliance issues. Moreover, regular reviews of customer data against updated KYC requirements ensure businesses remain on the right side of the law, potentially avoiding hefty fines for non-compliance.

Implementing efficiencies with AI/ML

Leveraging AI and machine learning technologies can drastically improve KYC efficiency. AI-driven systems are adept at handling large volumes of KYC data, learning from it, and identifying patterns that might indicate fraudulent activity.

Plus, these systems can also continuously adapt to new types of identity documents and evolving KYC regulations, reducing the need for constant manual updates.

Investing in comprehensive training programs for staff

While technology plays a crucial role, the human element cannot be overlooked. Investing in comprehensive training programs for staff ensures everyone is up-to-date with the latest KYC protocols and can effectively manage your KYC system.

Now, we did mention that staff costs can already be a heavy load to bear. But the flip side is that well-trained personnel are better equipped to handle complex cases that might require a nuanced approach beyond the capabilities of automated systems. As a result, you’re less likely to end up with a costly accident.

Embracing digital transformation for KYC processes

Embracing digital transformation is key to reducing KYC costs. This includes adopting digital identity verification solutions facilitating a seamless customer experience while ensuring security.

Microblink’s AI-driven solutions are designed to capture, extract, and verify identity document details accurately, helping companies scale competitively without compromising compliance or customer engagement.

Big takeaway

KYC costs are driven by the need to combine thorough identity verification with cost-effective processes. Organizations can achieve this balance by incorporating AI-driven technology that streamlines the verification process, reduces manual labor, and adapts to regulatory changes with agility. Ready to optimize your KYC process without compromising on compliance? Contact us and discover how our AI-enabled solutions can significantly reduce your KYC costs while keeping you ahead in compliance.