2025 Trends in Identity Document Verification: On-demand webinar

Webinar Overview

As we approach 2025, the identity verification landscape is experiencing rapid change and facing new pressures. In a recent webinar, Rex Robinson of Microblink spoke with Will Charnley, Chief Operating Officer at Liminal, and Albert Roux, EVP of Product at Microblink, about the top trends and challenges shaping identity verification. They discussed the rise of AI-driven fraud, the importance of verifying identities beyond initial onboarding, and the growing need for tailored solutions that address age verification, regulatory compliance, and user trust. In this blog, we summarize their insights and outline what organizations should anticipate as they navigate the road ahead.

Full 2025 Trends in Identity Document Verification Webinar

Full Transcript

Rex Robinson: Hi, everybody! Welcome to our webinar today. We’re just going to give folks a couple of minutes to join, and then we will get right started.

Rex Robinson: Wonderful. Hi, thank you to everybody for joining us today. We’re really excited to be talking about what’s coming up in 2025 in identity verification. Today we’ve got a a fantastic lineup of folks to share some of the latest insights.

Rex Robinson: So we are joined today by the wonderful Will Charnley, who is chief operating officer at liminal.

Rex Robinson: Will comes to the table with extensive experience in cybersecurity, financial crime, compliance, trust, and safety, so really running the full gamut. And he’s bringing these strategic insights into the operational and technical challenges of fraud prevention. We’re also joined today with Albert Rue from microblink leading product.

Rex Robinson: Albert has more than 20 years of experience combating fraud and developing cutting edge identity solutions, so really kind of keen to secure platforms and provide seamless digital ecosystems. And so these 2 folks today are going to walk us through what to expect and what are some of the key trends on the horizon in document verification for 2025.

Rex Robinson: Just a bit of housekeeping before we kick off. We’d love for this webinar to have a little bit of interactivity as well. And so you’ll see that there’s a Q&A function. Please feel free to drop your questions in the chat throughout the webinar. We will have some time at the end of the webinar to go through those that Q&A.

Rex Robinson: And then, lastly, this webinar is going to be recorded. So you’re welcome to watch it on demand after the time as well.

Rex Robinson: And with that I will hand it over to Will to kick us off. What is the lay of the land as we are wrapping up 2024.

Will Charnley: Awesome thanks, Rex, for having me, and for a great introduction, and super excited to be with the microblink team, and especially Albert, a very esteemed colleague on this panel as well. So I’m very excited to get going on some of the trends that we have.

Will Charnley: So we’ll start today off just, I think initially, a little bit broader, which is, you know, what we’re talking about today is really identity document verification and where the market is headed there, so I won’t spend too much time on this slide. I know, for many folks here, right, this is not going to be super surprising hopefully, which is that, you know, we have been moving over the last gosh, 20 plus years from a physical first environment. So if you think about, you know, how you, you know, historically have interacted with businesses as a consumer, right, going into bank branches, going into, you know, at one point, maybe a physical mall to go to stores, you know, even grocery shopping at the actual store. We’ve been moving more and more towards a digital environment. Obviously, covid accelerated that pretty rapidly, and we’re to the point today where most consumers open and interact exclusively with at least 20 plus accounts every year in a digital way. And so what we’re really gonna be talking about is, you know, as you see kind of on this slide, we are at this point where, you know, 83% of people have a preference for only interacting with businesses in a digital way, 82%, which is, you know, four fifths of the population, are pretty familiar with identity verification as a process to create that account. That would be a database check, that would be a document verification, that would be a selfie to document match. So there’s high familiarity with identity verification, the techniques, it’s being used today. And so, you know, all that leads us to this point, which we’re really going to spend time talking about today, which is, so where is this market going? What are the changes? What are the innovations that are happening and what makes us really excited?

Will Charnley: Hopefully, the last slide is very straightforward. But where we’re seeing the market going is that there’s a lot of change and a lot of opportunity in the identity verification market in particular. While, you know, we’ve seen rising demand for verifying an individual’s identity, what we’re seeing is that buyers need better built solutions depending on their pain points, depending on their use cases, to meet consumer demand when it comes to privacy, when it comes to security, when it comes to user experience.

Will Charnley: And so if we think about the history of identity verification, I’m just gonna give you a little history lesson, then we’ll speed right up to this. You know, many identity verification providers—actually, we track about 3,500 companies and over 300 identity verification providers—92% of those providers historically have focused on financial services. In doing that, most of those solutions have really focused on compliance centered solutions, right, identity is a part of what we would call know your customer, KYC. And so when you look at these 2025 trends, the big overarching theme here really is, many are noncompliance focused. Where we’re seeing this market go is that it needs to evolve outside of compliance to get better solutioning in many different ways. So first, and we’ll dive into each of these more deeply, while Gen. AI fraud has been a major pain point everywhere, one major area for concern we’re seeing is account opening fraud, especially in what we would call synthetic identity creation, which we will get into here in a bit.

Will Charnley: Second big trend we’ll dive into here, while identity verification has long been the gold standard, as we saw on the last slide, for account opening, we are seeing more and more use cases, for example, account recovery transactions, especially when it comes to age restricted goods that really not only benefit but really are going to start to require identity and verifying identities as a key component to creating a good solution there beyond kind of that day zero onboarding moment.

Will Charnley: And third, and this goes back to that compliance point, while buyers in other markets have long used some sort of identity verification solution, we are seeing more and more demand both from the consumer saying, “Hey, I need something built for this experience,” and from buyers alike that they need tailored solutions to meet the specific use case, and what we would call market use case. So use case plus vertical. So not KYC for banking, identity verification for vertical X. So we’ll be diving into this. But before we start really going deep, Albert, you know, I know you spent the last, you know, decade plus really building solutions and innovative solutions in the space, you know, how have you seen demand evolve product roadmaps evolve, shift over time to kind of get to this point? I’d love to hear your perspective.

Albert Roux: Yeah. Well, I think what we see generally across the industry is the demand from customers to have more than just a point solution. I think the main aspect for customers, what they want to do is to be able to depend on one or two vendors that actually can cover their use cases, and point solutions right now are reaching their limits, right? So, for example, if you just have vendors that provide only document verification, you know that for you to be able to just comply with regulatory requirements is to also have biometrics, database checks, device intentions, we have your biometrics. So how do you combine all those capabilities, but also leverage the data that they expose for you to essentially obtain, for example, a risk score?

Albert Roux: And that what we see is that now customers start to realize we want to have a platform which we can gain the insight of what’s happening from the user onboarding stage, and also add additional metrics, for example, pass rate or drop off rates that they’re able to leverage via those platforms. So the rise of analytics is also becoming a reality for many of our customers, and they want this in a centralized platform, a centralized point. So what I see generally is a shift now of looking beyond just a point solution, but looking for vendors who can actually cover end to end, not only the entire workflows, but also handle new threats, and for the new trust, in particular with synthetic identity, fraud, or Gen. AI, you’re going to need a combination of things. So how do you do that? You need to be able to drive this via an orchestration platform. If you don’t have it yourself, building a house, which is the majority of our customers, you’re going to look for someone who can provide that solution.

Will Charnley: Totally, and I think that’s—you got my segue down. This is perfect. I think it’s a perfect segue into this piece, which is, you know, our first big trend we’re diving into is around fraud.

Will Charnley: You know, unfortunately for many of the folks on this call who are, you know, buying solutions to combat fraud, the reality is the market is getting harder and harder. It’s more challenging to prevent fraud than ever right now, as you see in the slide, we’re predicting that synthetic identity fraud is poised to more than triple by 2030. So losses are expected to go from about 30 billion today or yesterday, I guess 36 today, to over 100 billion in losses. So things are clearly getting worse on that front. And as Albert has mentioned, I think you did a really good job here, which you know, why is this happening? You know, the reality is generative AI has made committing fraud incredibly obtainable, easy, and the quality has gone way up. So we’ve had higher volumes of fraud, we’ve had more sophisticated fraud attacks, and it’s more accessible to anyone. A good example here, there’s a site called Onlyfakes, and for $10 you can make a synthetic document. That’s it. You don’t need any training, you don’t need to be a computer scientist, you don’t need any programming skills at all. You just need $10 and the ability to pay.

Will Charnley: And the unfortunate part is, you know, the sophistication is so good it’s actually changing the way folks are dealing with fraud. I was talking with a practitioner the other day, and they had to change their fraud models because how they now are preventing fraud is they’re taking some of the best documents that they’re seeing and saying, “Hey, wait a minute. These ones are the actual fraudulent documents because they’re too good.” So, you know, the quality is such that they’re actually better than the real thing.

Will Charnley: You know, some of the areas we call out here, right, AI enabled fraud, obviously folks are preparing for it to be a huge, you know, 88% to grow substantially over the next 2 years. And I think even more alarming on this slide is 92% of buyers do not have a solution they feel like they can rely on to prevent generative AI attacks, deep fakes, meaning that they know something’s coming, and they know they’re not prepared for it.

Will Charnley: You know, Albert, I always say you’re kind of the leader in this space when it comes to strategies to prevent fraud. I know you started to talk about some of them, but what would you say to some of these, you know, 92% of practitioners that are kind of unsure of where to start when they’re preventing fraud?

Albert Roux: I think the main area is to realize that they probably have more fraud than they think they have. I mean, when we talk to customers, they tend to think, especially ones not exposed to it, but simply when we look and we review samples of documents that we verify, for example, we can recognize faults that our clients don’t even catch. And the main aspect is for them to first conduct an audit, if possible, with document experts or biometric experts to look at the extent of the attacks they are suffering from. I think that would be my first recommendation.

Albert Roux: The second step is, of course, looking for vendors that look at fighting the problem from different aspects, right? And how do they combine different capabilities together? I think that’s really important. For example, for Gen. AI, people tend to think the main risk is the new ChatGPT who can generate synthetic identities, but in reality, it goes beyond just curbing a ChatGPT ability to generate fake data.

Albert Roux: You have to look also for ways to detect what we call the risk of foundation models for machine learning that can generate video almost in real time—filters, for example. So there’s a need for the new products that you’re using to detect fraud, to look into the liveness of a document, for example. Computer vision models need to be adapted to improve on detecting whether or not a document presented to you is live, and does a person hold a real document. I think that’s one of them. That’s true also for biometrics as well, and adds new combinations of products that are existing on the market. So device intelligence: how do I tie a fingerprint to the document and to the biometric? And now how do I validate that information and make sure they are bound together so next time the customer comes back and we already verified that he’s legitimate, I can reuse that information or just add a minimum amount of friction?

Albert Roux: So those are the kinds of things that I think they need to think about and plan for, because if they don’t know, they are probably already suffering a lot of fraud if they don’t realize it. I think there’s a statistic out there that 54% of the current crypto marketplace is already being bypassed essentially by fraudsters just because they don’t have the right elements to detect fraud, right? So I think the combination of those different tools are not being put together today in the market.

Will Charnley: I think that makes total sense. And I love the idea. I think you really need a layered approach here. It’s not one thing that is solving everything. I think you need to really understand how to layer things in. But, Rex, I think we have some poll results around this. I would love to maybe dive in there if we can.

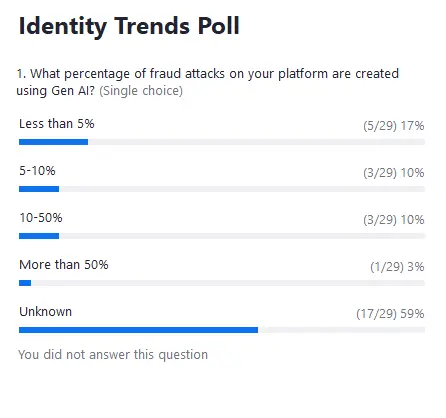

Rex Robinson: Yeah, absolutely. So we’ve been asking folks, you know, what percentage of fraud attacks on their platform are created using Gen. AI. So thanks to everybody who has participated there. So let’s take a look at what we’re seeing in terms of results.

Rex Robinson: So I think, unsurprisingly based on this conversation, there’s quite a small percentage of fraud today using Gen. AI of folks who responded. But really the majority here are folks who don’t know what their platform is. Is that sort of what you’d expect to see, Will and Albert?

Albert Roux: Doesn’t.

Will Charnley: Yeah, I’d love Albert’s opinion. The unknown piece, I think, is super interesting. Albert, what’s your take there?

Albert Roux: And the reality is what I was saying earlier, what I recommended: conduct an audit with the document expert just to start if we are just zooming in on documents. Generally, most clients don’t have the expertise. I mean, how do you recognize it? I mean, the majority of the pictures that we capture on the net, so the quality is not very high in reality, right? I mean, there are not that many pictures being captured in 4K, for example. And if you’re not a document expert, are you going to know whether or not that driver’s license being presented is real?

Albert Roux: You saw in the news recently that case where the United Healthcare CEO was killed by someone who used actually a fake ID to register in the hotel, and in my eyes I can recognize immediately it was a fake ID, but that fake ID was held in somebody’s hand, and that person did not even recognize that it was a fake driver’s license.

Albert Roux: The reality is, the majority of people don’t realize this is fraud because you need to have some level of expertise in document examination. That’s the reality.

Will Charnley: Yeah, totally. And I think complicating it is, you know, synthetic identity, the word is a little bit of a misnomer in that people think it means every part of it’s fake. That’s usually not the case, right? It’s a combination of fake and actual, real verified data. Right? Oftentimes, an address can be right. It might be a right social, just not the right combination of social, DOB, name. And so, you know, you might be verifying parts of this or getting a score that says, “Hey, this is passable,” which really actually is a synthetic identity. Yeah, I think that’s one of the more challenging pieces of it.

Albert Roux: Oh, sorry. I was just about to say it’s telling something, right? It simply means we don’t know the type of fraud that we’re facing because we’re unable to recognize what is fraud and what is actually a genuine user at this point.

Will Charnley: A hundred. Yeah. And I think the point you made, Albert, about like you need to get a baseline first, like step one is, you have to understand the extent of the problem. I mean, it’s hard to deal with a problem if you don’t know where you’re vulnerable, what’s happening, you know, what the attack is looking like, and I think that’s a really great point there on that front. I think we found especially synthetic identity to be a massive issue in studies with buyers. Eighty-nine percent think it’s a significant to very significant issue as part of their business.

Will Charnley: And I think the really interesting part here, the eighty percent to us is folks are actually planning to use more bespoke or tailored specialized solutions for this. Albert, I know we have to move on here to the next topic, but if you were to say, “Hey, these are the kind of one or two things you should look for in a specialized solution,” you know, what would your recommendation be to buyers in the room?

Albert Roux: I mean, when it comes down to synthetic identity, I think you have to couple document verification plus at least a database check. Because synthetic identities, the concept is very simple—you take different elements of real data, mix them together, and then you create a Frankenstein identity. So now something just as simple as verifying somebody’s address would be helpful, because is that person really residing there? At least that could be an indicator. Social security number verification could be another way to do this. But even social security numbers are being manipulated with synthetic identities. So essentially, I think the easiest way would be to have a simple database check.

Albert Roux: After that, of course, liveness—that’s also an important key point to have in your element. But, in short, as I mentioned, it’s a combination of different elements that validate the information being presented to you via a document or via biometrics. And what they should be looking into your vendor for is a vendor that is able to combine those different capabilities, but also enable them to measure the effectiveness of those defense mechanisms as well. So that will be something I will recommend to curb this product.

Will Charnley: Yeah, absolutely. Just moving us along because we have another T to get through here. So the next big thing that we’re calling out as a trend as we head into 2025 is the importance of identity beyond account opening. So first slide, that slide we all saw where everyone’s familiar with identity verification and document verification in account opening, you know, that has long been a process that people are familiar with.

Will Charnley: What we’re starting to see emerge is a need for these solutions beyond that day 0 account opening event. What we are finding is because there are rising fraud threats, which we’ve covered to some extent, there’s increased need for transaction security and authorization. If you’ve been following any of the things that have been going on with Zelle and the government, and the need of ACH, wire fraud, etc., as well as new use cases emerging like age assurance, identity is really something that is needed more and more to tie whatever it is—the transaction, the token, if it’s in login—back to the actual person who’s doing something.

Will Charnley: Additionally, what we’ve seen is, you know, as new modalities are starting to emerge in other parts of the customer journey—example here being something like passkeys—identity can play a really crucial role in ensuring the security where other modalities like SMS OTP, like email OTP, have not really done a good job and are becoming less secure for folks.

Will Charnley: Albert, I know you work with a lot of customers, you know. What are some of the needs you’re hearing from folks for, you know, identity beyond kind of that initial account opening moment?

Albert Roux: Yeah, beyond the initial onboarding, I think a lot of customers are worried about account takeover. I think that’s one of the main risks because of generative AI and synthetic identity, but primarily because of generative AI. Imagine now I can fake your biometrics—so your face, your voice, and your documents. That means that someone can now access your accounts relatively easily, right? So I think that’s one of the biggest concerns customers have is, how do I protect myself against account takeover?

Albert Roux: The second concern I think that I do foresee, I mean beyond, it’s authentication in general, as you mentioned. I think that’s the biggest concern. But also with a new regulation coming into place, especially for social media access, age verification. So not only for social media, but restricting goods, for example—that is, how do I verify someone’s age and how do I verify it relatively accurately, which is a challenge, right?

Albert Roux: So I think right now, our customers are widely spread out, at least for Microblink, beyond just banking and financial services. So that also concerns not only customers who are subject to regulatory compliance, but also other customers as well. They are worried about the same threat.

Will Charnley: Yep.

Albert Roux: Oh, go ahead. Sorry, Will.

Will Charnley: I was gonna say, the age thing—I know we’re going to get into it also in a little bit—but I think that is, I think, even more kind of squarely where regulation is really accelerating. Australia’s social media law that came out—it might have been two weeks ago at this point. Time is all relative, this close to the holiday.

Will Charnley: But I thought that was really telling, and we’ve heard from a lot of other folks in governments around the world that they are considering similar type regulations. Which would obviously, I think, very vastly accelerate the need for age solutions for sure.

Will Charnley: I think we have, Rex. Is it up, or should I flip to it? A poll is coming up here.

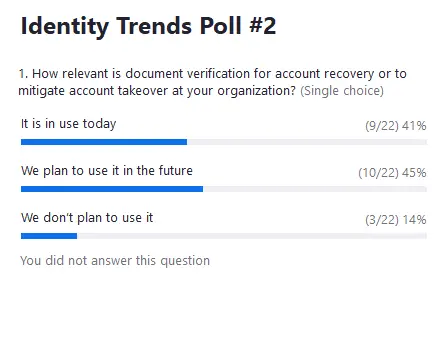

Rex Robinson: Yeah, I’ll launch it right now. So we’ve got another poll for our audience. Love to hear from you all how relevant document verification is for your account recovery, or to mitigate account takeover at your organizations. I’ll give you all a second to respond. We’ve already got a couple of answers coming in.

Rex Robinson: And I’ll just take this moment to mention as well: we’re seeing some great questions come in the Q&A. Feel free to keep adding your questions there, and, as I said, we will take some time at the end of the webinar to answer them.

Albert Roux: And then, while we’re waiting for the poll as well, one thing I wanted to mention, we cite email and SMS OTP as traditional ways to authenticate users. I think what’s important now is when you consider an ID vendor: do they offer biometric verification? Do they offer multifactor authentication beyond just SMS OTP? I think that is also important to consider.

Will Charnley: A hundred percent.

Will Charnley: You know, especially along the lines of biometric authentication. We did a very large customer authentication report. Number one area folks were looking for from a buyer perspective as a way to secure their authentication was biometrics. The biggest challenge they found was account recovery. So, you know, I think biometrics can play a key role in both of those areas for sure.

Albert Roux: And then you also have device intelligence—essentially tying your personal device to an identity. I think that’s really important for you to integrate. If you’re a merchant or a banking institution, it is important to recognize: I’ve seen that user before and make sure that their device and their profiles, the ways they interact with your application, can help you determine it is the same person. So those are the things that you should absolutely use in combination as well. Something just as simple as a device intelligence product can tell you: Is that person even in the same geography when they are trying to access your account? That is a very simple check you can do via an IP address check, and that should be enforced at a minimum in your workflows.

Rex Robinson: Let’s go ahead and look at the results of the poll.

Will Charnley: I love it. I love it, Albert. I don’t know about you, but I think these are great results, and I think they point to a lot of the folks here actually being at the forefront. You know, when we’ve done studies and what we’re showing on this slide is, you know, a year ago not many folks were doing this, and we’ve seen a massive acceleration of adoption, right? Going from 8% to 23% is huge. I mean, that’s a big increase. And it still means this market’s pretty nascent. So, Albert, I don’t know if you feel differently. But the 86% of folks who are doing this or plan to do it soon, I think that would be our recommendation, and now is the right time to act. Albert, I don’t know if you have a different reaction to the poll, but that’s my first glance there.

Albert Roux: No, I think it’s a known thing, right? Because now on top of this, IDs are getting digitized. So now you’re going to have digital copies of your identity documents. I mean, that makes things even simpler for you to authenticate documents, which will be a thing. So you definitely want to have this in your arsenal when you check someone’s onboarding or accessing an account. And also with a database check, some of them are relatively robust. You can add this on top of your document verification without adding any friction, because you’re talking about milliseconds essentially to do this. So I am not surprised by the trend, and I think that’s a good sign.

Will Charnley: Yeah. And I think what we call out on the right side, it’s not just ATO, it’s not just account recovery, although those are two big areas. Especially account recovery. And you mentioned SMS OTP, that is a huge vulnerability. There’s also the other side of the coin. You know, my wife got locked out of her bank account, and it was a call center. The password reset was at the call center, and that is also not the most secure, because there are plenty of different ways to defraud that process. And also, you talk about friction—going into the branch is probably number one and number two has to be call center. So, you know, balancing security with user experience, there’s not many better ways to do that than really by verifying someone’s identity digitally.

Will Charnley: Some of the other areas that we found a lot of demand for folks here—it’s worthwhile to definitely explore ATO and authentication, especially when it comes to authentication moving beyond just tying a token back to a token. Like, you know, your Apple iPhone isn’t necessarily verifying your identity when they’re doing that initial biometrics; it’s easy enough to replace the biometric modality there. It’s actually secured with biometric authentication back to the identity. And then the last piece here, which I know we touched upon, and we’ll talk about even in the next piece: age is a big use case. And then, lastly, we didn’t show it here, but we are seeing a bigger need for identity in transactions as well, specifically high-value transactions.

Will Charnley: There’s—there was—the government actually has started to try to put a lot of regulations in place for folks like Zelle, for a lot of these peer-to-peer payments, for ACH, wire transfers as well, because there’s a massive challenge around social engineering where folks are sending money and then have no way to reclaim that money, even though they’re being defrauded.

Will Charnley: Historically, financial institutions have not been liable for those transactions, but there is a lot of movement and talk to have them and—and make them actually need to put processes in place. So I think we’ll see a lot more use cases where this is becoming really, really important.

Will Charnley: And with that, move us to our 3rd trend, so we stay on time here, which is—

Will Charnley: This last, you know, our last trend is really around how and why solutions are shifting outside of financial institutions. So, you know, without going back and giving the history lesson I gave earlier, identity verification, identity document verification has long been used in financial services. That’s where many, many folks started when they created solutions. Identity verification has moved into adjacent verticals. I’m assuming many folks here have probably gone through either a flow where they have verified the identity on platforms like Linkedin, or for an online gambling site, or etc., etc.

Will Charnley: You know, many times as these solutions have expanded into new verticals, practitioners have been, you know, kind of tasked or forced, however you want to look at it, with using a compliance-first solution, a solution that was made for banking with a different wrapper, and then said it’s being used for a noncompliance use case like identity verification on Linkedin. You know, example: here I was talking to a very large marketplace doing business verification, and they told me they needed a KYB solution.

Will Charnley: They do not need a KYB solution, or know your business solution. They don’t need to do ultimate beneficial ownership, they don’t need to do many of those manual processes that cause verifying a business for banks to be weeks or a week-long process, a very expensive process, and that just doesn’t fit outside of financial services. The result of a lot of these misfit kind of solutions of, “Hey, we’re using a compliance solution for a noncompliance use case,” unfortunately, is shown on this slide, which is a ton of pain points when it comes to the consumer. So these results actually come from a large consumer survey we did explicitly, looking at folks outside of those financial services verticals.

Will Charnley: Two big things I’ll call out, and then, Albert, I’d love, you know, your opinion here as well, which is, you know, the first big one is 31%, you know, using kind of these misfit solutions, right? Thirty-one percent had significant data privacy concerns, many times because they were asked to provide a lot more data than they actually felt like they should have to be, which makes sense, because they’re providing data you would need to open a bank account, not data or documents that you would expect to use to open a marketplace account or a social media account, as an example.

Will Charnley: Second big thing is we bucketed some of these together, which is, you know, too much friction, too much time. There’s a lot of UX concerns. A lot of folks are abandoning account opening processes. It’s actually about 57% of folks felt this was a huge issue, their number one issue when opening an account outside of financial services, again, because they’re using solutions not really tailored for the use case themselves.

Will Charnley: You know, Albert, I think, you know, data privacy is a big one here. It stands out as a big concern. You know, what are you hearing, kind of, from the market on that one?

Albert Roux: Yeah, I mean, I think right now most customers are always worried about data privacy, especially with lawsuits that we’ve seen in the US in regards to biometrics lately. I think what’s really important to our customers is collect only the data essential to perform the check, discard that data as quickly as you don’t have a need to do it, and at the same time, we want to make sure we retain the same level of accuracy when we determine whether or not the person is a fraudster or genuine essentially. And at the end of the day, it’s really trying to balance the level of data that we capture, or at least maintain a certain level of privacy for the end user, while, of course, still ensuring that your product is accurate when making that determination.

Albert Roux: But also what we see with a lot of customers, at least the type of customers that we have, including into regulated areas, is that they want a higher pass rate, right? Today, actually, unfortunately, I would say probably the pass rate for a lot of financial institutions, a basic account opening even on e-commerce, you’re looking at something between 50 to 60%. I know a lot of companies claiming a higher pass rate, but what I observe over the last few years I’ve been looking at data is the pass rate is not that great. And why? It’s because the majority of fraud vendors are not optimizing towards this, right? There’s very few companies out there that literally dedicate their efforts to ensuring your SDK screens make sense, are easily usable.

Albert Roux: So, for example, in our document verification at Microbik, we can do a document check in less than 3 seconds right now. What we’ve seen with other vendors is that it takes up to 30 seconds. In some cases, I’ve seen up to 2, 3 minutes to do that, and that’s when users start to become discouraged because they are facing an interface that they are not familiar with, and they drop off. And so, in reality, when you craft a product for identity verification, privacy, of course, needs to be by design first, but also usability of your product. And that’s why we invest heavily into that area of design, because it’s really important for our customers to see the highest possible pass rate.

Will Charnley: 100% agree with that piece. Yeah, pass rates—I think people, buyers are oftentimes very shocked, right? You go on a website and it’s 99.9% or some unobtainable number, and then in practice, I think people see the reality, you know, when customers and their specific customers are actually using a solution, results can be really different. All the more important to make sure you’re choosing the right solution for the customers you’re trying to work with, and the use case.

Will Charnley: And so I think we’re gonna flash up a poll here, too, as we go through this. But you know what this all means, and we’ve been talking about this, is that you really need to, as a practitioner, make sure you’re buying a solution that fits your specific needs. Why we’re breaking this out is the way we at Liminal see use cases—we call them market use cases, the market being a vertical or industry. And the reason is really laid out on this slide, because even if you’re solving account opening, depending on your industry, who is buying that solution, the persona, the actual requirements that you’re looking for that solution to do, the KPCs, the key purchasing criteria that you care about, and some other considerations are going to be vastly different. Right?

And so, if you are a chief compliance officer at a bank, you are going to be buying a very compliance-centered solution. You typically know what you want, right? You want to do things like perform customer due diligence, submit regulatory reports. If you are the head of trust and safety at, you know, an Airbnb-type company, you don’t need to do those things. What you really need to do is make sure that you are enhancing user trust on your platform, because that will lead to more booked nights and better experiences. You need to be able to do other different things like potentially verify age or do more risk scoring, do more safety-type screening from a trust and safety perspective. And how you want to buy solutions might be really different.

And so, if you are, you know, kind of looking at, “Hey, I’m more on the right side of this slide,” you should be asking your practitioner how they’re helping you solve some of these use cases. In particular, you know, for age, which I know we have up on the screen here, right? I think there are different ways to verify age, and finding the right size for your use case is incredibly important.

Rex Robinson: Yeah, absolutely. Let’s take a look.

Will Charnley: Interesting.

Will Charnley: Albert, not to put you on the spot, but what do you make? I know you’ve spent a lot of time in the age verification space.

Albert Roux: Yeah, I think I tend to agree with the results of the poll, right? I mean, the reality is the majority of solutions currently on the market for age verification will rely on a user or computer vision-based system. So analyzing somebody’s face and trying to guess what age range they’re in, and unfortunately, that’s widely inaccurate at this point of time, right? There’s not that many good solutions out there. So we have to look at different alternatives to this check. You can extract information from a driver license and then check that information. Make sure that it’s accurate against some database, for example, Amva. You can obtain the age of a person, but that’s not sufficient today, right?

So for us, we’re looking at what are other ways beyond just document and biometric or systems based on computer vision. So one thing that can be simple is, for the U.S., for example, you can establish somebody’s having a credit card or debit card. In the U.S., that means that you’re over 18. So that could be something simple as this, and then on top of this, extracting that information off the debit card to make sure that it’s a valid debit card, but also has a liveness of that document, right? So looking at the document in terms of verification and biometric could be a way to quickly validate age verification cases potentially, right?

So those are alternatives that we can look at on the market. There’s also a solution, of course, but primarily these days it’s going to be either a database check, a biometric check, or a document verification. The alternatives that we offer at Microblink is via our Blink Card product that is used by companies—I mean, for example, if you look at Google, that’s how they verify that someone is over 18, by just asking the user to show their debit card. So I think today’s solutions are not sufficient. There needs to be further refinement in that aspect.

Will Charnley: Yeah, I think that’s a great point as well, to the point you’re making, which is in reality, especially when it comes to things like age, having different types of solutions depending on the risk is really important, right? And you know, I think the example you gave me with Blink Card is a really good one, which is also tailoring your solution to what folks are likely to have. So if you’re making a, you know, an e-commerce transaction, you should and likely will have your card with you. You might not have your identity document with you, and so being able to do things off that card is important. But also layering in technology for some of those pieces, which is, you know, in no circumstances is probably a still picture going to be acceptable, you know, way to do that as well.

Albert Roux: Yes, and also triggers those checks whenever you need it. You don’t need to always trigger those checks at onboarding. You can also trigger them, for example, in a credit card-not-present. So for banking institutions, they do require biometric. But if you’re an e-commerce platform, do you really need that biometric check? Unlikely, right? Some kind of document check or debit card check for high-risk moments where a transaction seems to be abnormal. So that is how we work with our customers to tailor a little bit, because in reality, most customers try to take what is done on the KYC side of the house and just port them over. That’s not ideal because it needs to be a bit different. So use cases are different, so it needs to be.

Will Charnley: Yeah, a hundred percent.

Will Charnley: Alright, with that, I think we want to get to questions. So we’ll wrap up this piece and get to the Q&A, which is, you know, alright, based on all that, kind of what is the so what here? What should we actually kind of take away?

Will Charnley: So three big points here, you know, both off of the terrible icons that I pulled up— you’ll just have to live with those icons. First one, as it relates to fraud, I think having a really, really important for practitioners here to have a really honest conversation, not just around, “Hey, what are you doing from a compliance or identity perspective?” but “What are you doing for specific types of fraud?” You know, more and more we are seeing not only—it’s not just account opening fraud—it is specific vectors like synthetic identity where people are getting hurt the most. And so understanding where your pain points are, I think Albert’s suggestion is really a great one. You have to really start by understanding how big the problem is, where the problem is, and make sure that if you’re using a solution provider today, they’re the right ones to address that problem. I think, Albert, a lot of great points, but asking, “Hey, what are you using to combat synthetic identity? How is that different from what you’re using on the compliance side of the house to do a KYC check?”

Will Charnley: Second big piece here, as we get to beyond, you know, those day-zero onboarding—I don’t have to tell this audience because you guys are great and already planning to or are using solutions beyond account opening—identity, you know, if there are ones that came up today and you thought, “Hey, I’m not sure how to use that,” I think it’s worthwhile to explore where identity can help more securely do things for you or enhance processes for you, especially because beyond onboarding, account recovery, ATO, those are two major areas we are seeing massive issues where identity can significantly help prevent fraud, make better experiences for your customers, help retain some of those customers.

Will Charnley: And lastly, again, if you’re in financial services, you might not have to do this, but if you were saying, “Hey, I use a vendor because, you know, I asked my friend who has implemented that solution at Wells Fargo, and I don’t know if it’s right for me,” I think it’s worthwhile to explore what is the use case I’m actually trying to solve, what are the things that are most important to me, and making sure your vendor is helping you do those things. If it’s around age, you know, it doesn’t have to be a KYC check every time, right? Understanding how they are approaching that solution, how are they thinking about it in a more of a risk-based way?

Will Charnley: And with that, Rex, I think we’re gonna go to questions.

Rex Robinson: Yeah, as promised. Thank you all for your participation in the polls, as well as the great questions that you’ve been sending through. We might not have a chance to answer all of them in the 10 min that we have left today, but we will also be able to follow up with you all offline. So again, feel free to drop any other remaining questions you have in the Q&A.

Rex Robinson: But I’ll kick us off with the first one here. What are the differences between an identity solution that is suitable for an SMB versus a large enterprise?

Will Charnley: I can start us off, and then, Albert, I’d love your perspective. So I’ll just use financial services to start, and we’ve done a lot of studies with buyers of different sizes in that space. If you go talk to a tier one bank—and I’ll use an example here, like a Citibank or JP Morgan that has many multinational branches—they are more likely to have their own inner orchestration capabilities, existing vendor contracts. And so they’re typically going to be in setting up things by specific solution type.

Will Charnley: In some instances, if you have a big presence in the US and a big presence in Europe, you might want to use different vendors based on regional expertise for those areas. So, as an example, you might want a vendor who really has deep, deep expertise in the United States, especially direct connected data sources, so that you can ensure data quality, ensure accuracy. And then you might want someone in Europe or the UK who has that same level of expertise. That’s pretty common.

Will Charnley: We see that for large enterprise buyers, because the teams at those organizations are also very large. It’s not uncommon that just the cost for the team at those organizations is millions of dollars that they’re spending to have experts there. So you have the actual team who can implement 10, 20 vendors and integrate them all together and try to orchestrate them.

Will Charnley: That’s great for maybe the top 20, maybe the top 30 banks. Once you move beyond that, the team size shrinks pretty dramatically. The inner capabilities are typically not exactly the same. And so we see more and more that folks in those areas have a much greater need for solutions that can do two things. One is help with multiple use cases, especially in account opening, but also help beyond account opening. And so that’s where we see a much larger demand for platforms and for solutions that will work alongside those companies to help in other areas of the business. I know I just rambled on, Albert. I’m sure you have stuff to add there as well.

Albert Roux: Well, this was perfect, actually, because what we see with SMBs is they tend to have maybe one, two, three use cases at most, and their workflow tends to be a little bit less complex, right? Because, for example, they don’t have a human in the loop. So just when you conduct a basic verification of an ID, larger enterprises usually want to reverify that the system performs adequately, so they will escalate a portion of the checks to a human. That’s not something an SMB can do.

Albert Roux: Also, what we just mentioned is when you deal with your large enterprises, generally, they are global. They’re looking for a global solution, and they also want to have the ability to orchestrate workflows depending on the geo. That means a feature as simple as parent-child accounts is really key for a large enterprise, but it’s not that important for an SMB, because generally they don’t have a branch in India or Vietnam, or something like this.

Albert Roux: Also, the complexity of the checks. Large enterprises, especially the ones in regulatory areas, their workflows are extremely complex, and they demand a lot of different inputs in terms of signals, and then also the ability to centralize all the signals that they have and come down to a unique decision. So they are going to require biometrics, they are going to require document verification, device intelligence, all those different things, whereas an SMB might have simpler use cases, and therefore the workflows are not as complex.

Albert Roux: Also, the analytics part, even though both SMB and enterprises love to look at analytics, the reality is that the level of granularity of data that they can use is very different between large enterprises and SMB, right? So the sophistication on which they use data is totally different. So essentially, your platform needs to enable both, because we have some SMBs that are growing extremely fast, and they can become large enterprises within a year or two. How does a vendor adapt to the needs of their customers? We need to design a platform that can scale up. And essentially, that’s what you need to look for even as an SMB. Can you find a vendor, an IDB platform that can grow with you for the next 2, 3, 5 years? Right? So when we build our products, we have this in mind. We want to be able to grow for customers, and that’s how we design our identity platform.

Rex Robinson: Yeah. Fantastic question. The next question we have is kind of a two-parter. It’s really dealing with some of the pain points in the buying process when folks are looking to implement an identity solution. So here’s the question: What are the aspects of identity verification—document and biometrics—which cause the most amount of friction during the buying phase? And then the second part of that is what is the best way to navigate that, because many identity providers would prefer to have their own SDK deployed to improve capture, but that can then be a higher engineering cost for the business buyers, and then stretch deployment times. I’d love to turn that over to you, Albert, as a builder. What’s your take there?

Albert Roux: I mean, the reality is what takes the most friction, and I think the question here is in terms of integration. I mean, that’s as always, whether it’s an SMB or large enterprises. To give you an idea of how long it takes for certain customers to integrate an SDK can be anywhere from 3 months to even 9 months. I’ve seen even 12 months, just because sometimes they don’t have the teams who have the understanding of the technicalities to integrate another SDK into the application, especially mobile applications, even though we try to strive to make our integration as seamless and easy as possible.

Albert Roux: We can deploy on device, on premise, and on the cloud today at Microblink, but I’ve seen that even if we simplify the integration, sometimes they don’t have the team expertise. It seems sometimes it could be as simple as implementing one line of code change, but sometimes they simply don’t have the person to even vet once the integration is done. So I think the main friction point is really integration. SDK, I see the comments here, always takes a lot of time. It is the optimal solution, right? If you want to have the best possible product performance, an SDK is the best way to go. Now, we have customers who prefer web views, for example, but web views are notoriously unreliable from a technical point of view. So the friction time of integration is less, but downstream that causes a lot of problems of compatibility between different devices and OSs.

Albert Roux: The reality, to answer that question, is its integration regardless of whether it’s document verification, biometric, or any of the solutions. So one that has the least amount of friction would be an API integration type. But even that can also bring some challenges.

Will Charnley: Yeah, from more of a market perspective, I think there are just two quick things to consider. One is ensuring that the solution you’re using—maybe I’ll do three—is, when they say automated, is automated. It’s really important, right? There are a lot of solutions in the market that still rely heavily on manual review processes, which that’s a big cause of friction of queuing users.

Will Charnley: From a biometric perspective, I think it’s also really important to understand as you’re talking to vendors about their expertise with different population types. As an example, the same with documents. Do they have experience scanning documents and scanning faces with different device types? In the US, predominantly it’s iPhones. That’s not the case in most places. And also different types of people, right? There are models with things like racial bias, etc., which can cause a lot of friction when it comes to onboarding certain types of users. So it’s important to understand that the person you’re using for documents and biometrics has, especially if you’re looking globally, expertise within those regions. With a controlled data set, everything looks like it has no friction, but in practicality, it really depends on the customer base you’re working with.

Albert Roux: And also to add, it’s much easier to integrate a cloud-based solution than it is to integrate on-prem. Generally, we try to recommend our customers to go for a cloud solution. Yes, there’ll be a small component that relies on an SDK, because you still need to capture an image for document verification, for example. But the easiest way is really to integrate with a cloud solution, because the updates are coming much faster once you deploy. For example, every time we onboard a new document, then you don’t need to update your application. We support it on the cloud, and you have access to the latest and greatest models and document coverage. So I think that could help some customers to make a decision, is to look for companies who can offer both a cloud solution and on device or on premise. But I will generally try to guide the customers to adopt our cloud solution because of the ease of integration and scalability globally as well.

Rex Robinson: Great. Well, I think that’s about all the time we have for today. This has been a really, really juicy session. Thank you to everybody who has participated. The questions have been great. For anything that wasn’t answered on the call, we will make sure we follow up after the fact, and this webinar will also be available for you to watch again at your own leisure. So check out your email inboxes shortly.

Rex Robinson: Albert, Will, thank you so much for all your insights and for your time today. It’s been a real pleasure to have you.

Will Charnley: Thank you. Really, really appreciate you having us, this is great.

Albert Roux: Thank you, everyone. Bye now.