Understanding Customer Due Diligence Requirements

Customer due diligence (CDD) is crucial for building trust in the financial sector. It involves verifying customer identities and assessing the risks associated with doing business with them. This assists in mitigating financial risks such as money laundering and terrorist financing.

In this blog post, we’ll walk you through why customer due diligence requirements are essential for secure and trustworthy financial operations.

Regulatory landscape

The legal framework governing CDD combines international standards woven into national regulations. These global standards are set by bodies such as the Financial Action Task Force (FATF), which provides recommendations recognized as the international benchmark for preventing financial crime.

The impact of these standards is far-reaching as countries adapt their national legislation to align with FATF recommendations, ensuring a concerted global effort against financial crime.

Examples of key regulatory bodies include the Office of Foreign Assets Control (OFAC) in the United States, the Financial Conduct Authority (FCA) in the United Kingdom, and the European Banking Authority (EBA) within the EU.

Each body is responsible for enforcing CDD requirements, with the power to investigate and penalize non-compliant institutions.

Importance of customer due diligence in financial institutions

Understanding a customer’s risk profile is central to the CDD process. Financial institutions are tasked with conducting thorough background checks to identify the risk each customer may present. This means scrutinizing the source of funds, the nature of business activities, and any potential red flags that could indicate financial crimes such as money laundering or fraud.

Mitigating risks of money laundering and fraud

Effective CDD practices are crucial in the fight against financial crimes. Take the Danske Bank scandal, where insufficient CDD measures led to the laundering of billions of dollars.

In another case, the Commonwealth Bank of Australia (CBA) paid out a massive settlement due to a money-laundering scheme, which saw the flow of illicit funds due mainly to poor CDD measures.

Enhancing regulatory compliance

Robust CDD processes are not just about stopping crime; they also ensure financial institutions stay on the right side of regulations. By implementing thorough CDD measures, institutions can detect suspicious activities and preemptively address them, reducing the risk of costly penalties and sanctions.

Protecting the reputation of financial institutions

A financial institution’s reputation hangs in the balance based on its approach to CDD. A solid reputation for rigorous due diligence fosters customer trust and enhances the institution’s credibility. It sends a message that the company values security and is committed to upholding high ethical standards, which can attract more business and bolster customer loyalty.

Conversely, a poor CDD reputation suggests a lack of diligence and can raise concerns about the integrity of the institution’s processes. This can lead to losing customer trust and potentially invite scrutiny from regulators and the public. These days, where trust in online platforms is paramount, ensuring a positive CDD reputation is crucial for your long-term success and sustainability.

Key components of customer due diligence requirements

When dealing with CDD, financial institutions navigate a complex landscape to mitigate money laundering risks. The CDD process is crucial for identifying legal entity customers and developing a comprehensive risk profile.

It involves several key steps:

- Establishing the identity of beneficial owners

- Developing customer risk profiles based on a risk-based approach

- Conducting ongoing monitoring to detect suspicious activities

- Determining whether higher-risk customers require enhanced due diligence (EDD)

Let’s look at these components in more detail.

Customer identification

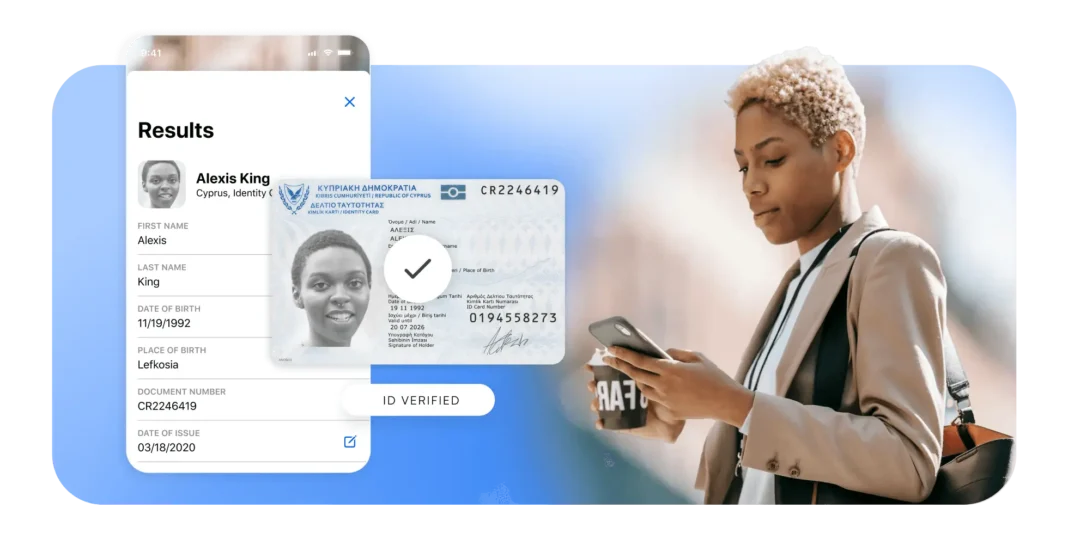

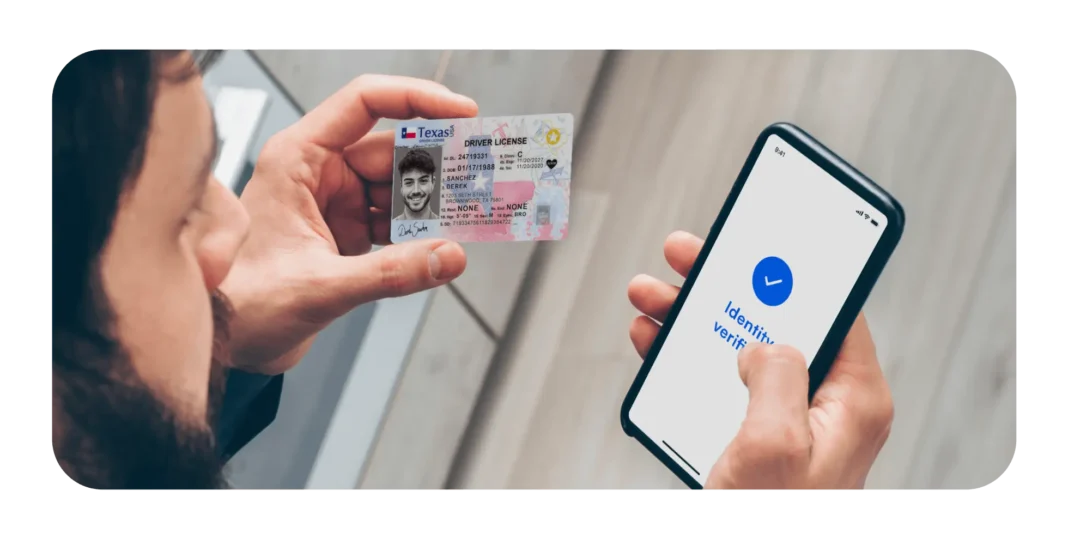

Financial institutions are responsible for establishing a customer’s identity, which involves collecting foundational information such as name, address, date of birth, and official identification numbers, like social security or passport numbers. This step is essential in the CDD process, where the due diligence process begins.

The spectrum of customer identification methods ranges from manual to automated processes. While manual processes may involve face-to-face verification or paper document collection, automated processes leverage technology to rapidly and accurately collect and validate customer data, streamlining your customer’s experience while maintaining rigorous standards.

Customer verification

Post-identification, the next critical step is customer verification. Financial institutions must ensure the authenticity of the information collected. This phase often involves confirming the validity of documents the customer provides, such as government-issued IDs or utility bills.

Integrating AI-driven solutions can significantly enhance the verification process, cross-referencing and confirming data against multiple sources swiftly and precisely, reinforcing the institution’s defense against fraud.

Risk assessment

Risk assessment is a pivotal component of CDD that necessitates a thorough analysis of each customer. Financial institutions evaluate factors like transaction history, the nature of business activities, and operational jurisdictions. This assessment is not merely procedural; it’s strategic, shaping the intensity of scrutiny and monitoring the customer will be subjected to.

The development of customer risk profiles enables institutions to tailor their CDD measures appropriately, applying a risk-based approach that aligns with the identified threat level.

Know your customer (KYC) procedures

KYC procedures delve deeper into understanding and verifying the nature of the customer’s activities, the origin of their funds, and the intent behind their transactions. These procedures are integral to detecting and preventing financial crimes, acting as a safeguard against the misuse of financial systems.

Through the KYC process, institutions gain insights that inform ongoing customer relationships and the continuous refinement of risk profiles.

Ongoing monitoring

Acknowledging that financial behaviors and risks are not static, CDD demands persistent monitoring. Financial institutions must keep customer information current, especially when substantial changes in financial behavior or personal circumstances occur. This ongoing process ensures the institutions remain vigilant and responsive to evolving risks.

Enhanced due diligence (EDD)

For higher-risk customers, institutions escalate their efforts into EDD. This level of scrutiny is more intensive, involving a deeper dive into a customer’s background, financial dealings, and the origins of their wealth. EDD is a rigorous process reserved for situations where the standard CDD measures are insufficient to mitigate elevated risks.

Meeting customer due diligence requirements

CDD is not static—it’s an evolving necessity that keeps financial institutions secure and trustworthy. It is essential for financial institutions aiming to mitigate risks and adhere to regulatory compliance.

The process involves verifying the identity of customers to prevent fraud and money laundering activities. As such, customer due diligence solutions are integral to the foundational integrity of any financial service provider.

How Microblink can help

Microblink revolutionizes this process by leveraging cutting-edge technology and AI-powered solutions. With BlinkID, Microblink automates the CIP programs, making identity document verification seamless, accurate, and swift. This automation translates into a more robust due diligence process for your business, allowing you to scale competitively and engage your customers more effectively.